SemiAnalysis Got Unitree’s Cost Advantage Right — the Supply Chain Is Where the Real Value Sits.

Lower blended margins, a manufacturing moat instead of a technology one, and 200+ competitors already using the same actuator ecosystem. The infrastructure layer is the smarter, more durable bet.

SemiAnalysis just published the best framing of the Chinese humanoid robotics market we’ve seen. You can read their piece here. The BYD/DJI analogy is correct. The BOM teardown is solid. The cost advantage is real and structural. But “dominance” is doing a lot of heavy lifting in that headline, and the data behind it tells a more complicated story than the piece lets on.

We’re not here to debunk SemiAnalysis. They got the big picture right. We’re here to go deeper on three things they didn’t fully unpack: what the margins actually look like when you use real selling prices instead of list prices, what’s inside the actuators that make up 66% of the BOM, and why the component suppliers, not Unitree, are the real winners of this cycle.

Thesis: Unitree's cost advantage is real and structural. But "dominance" is a timeline call, and the timeline depends on reliability data that doesn't exist yet, blended margins 12–17 points below the headline number, and 200+ competitors drawing from the same supply chain.

What SemiAnalysis Gets Right

Let’s give credit where it’s due. The BYD/DJI playbook framing is the cleanest lens anyone has applied to Unitree’s strategy. Own the most expensive component (actuators), bootstrap a willing market (researchers/hobbyists), ride the ecosystem, and let each hardware generation unlock the next market. That’s exactly what’s happening. The parallel to BYD’s battery-cell-first strategy and DJI’s flight-controller-first strategy is tight and well-argued.

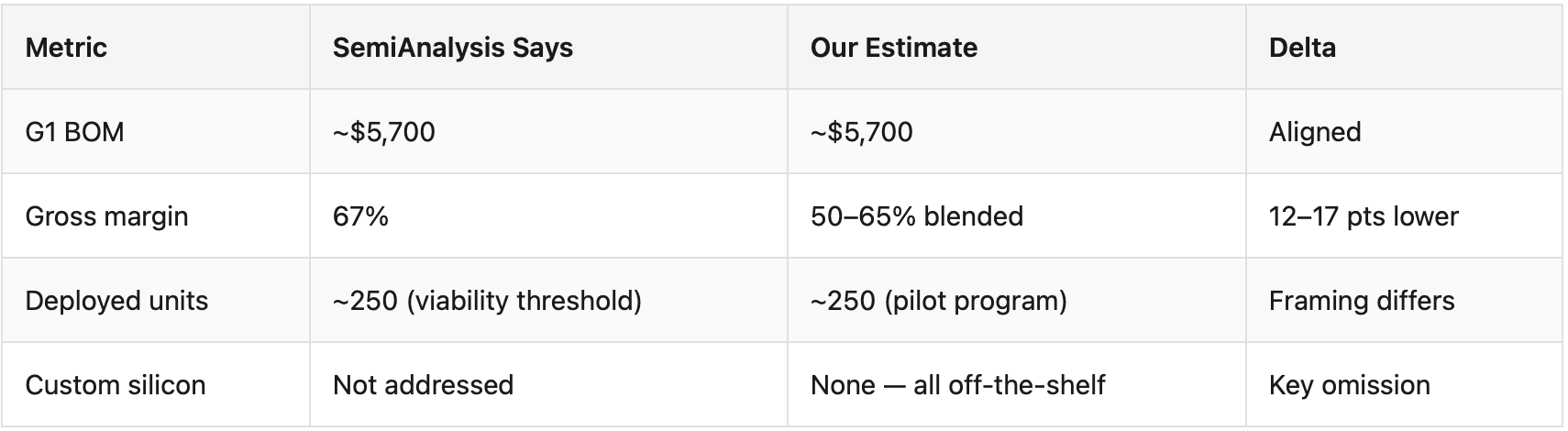

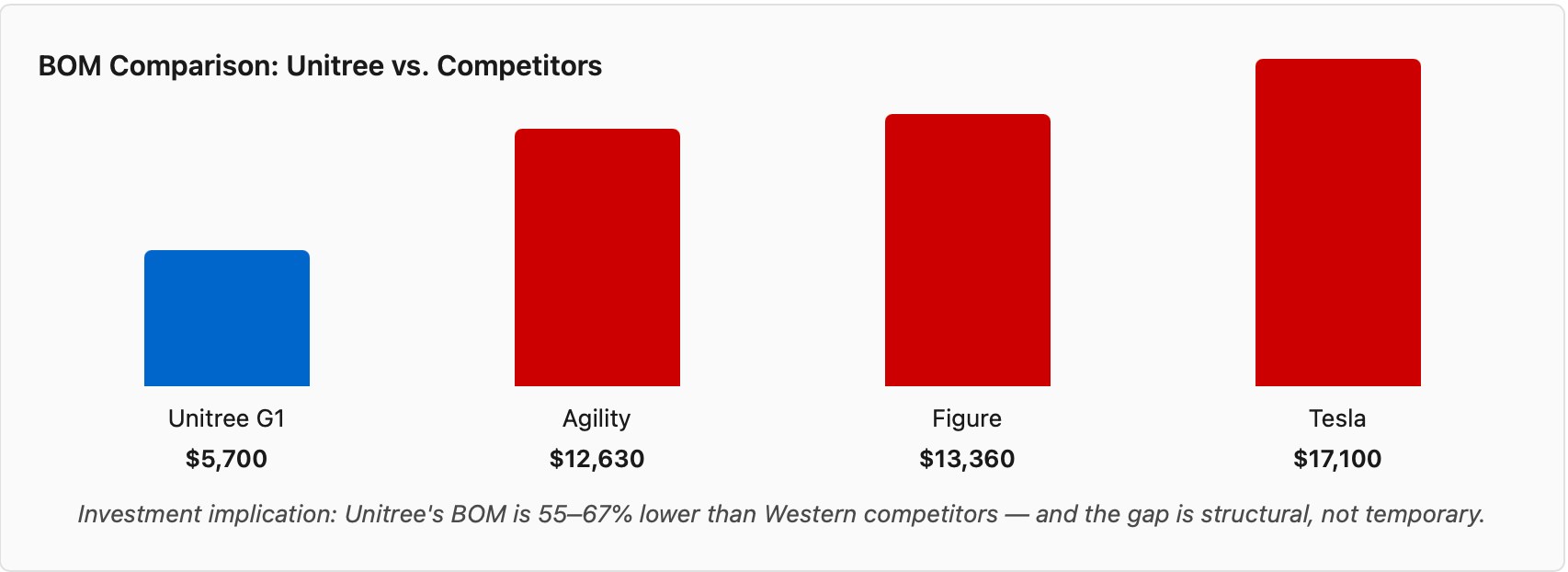

The BOM analysis is also correct. We’ve run the same teardown through CNP Securities’ data, and we land on the same number: approximately $5,700 total BOM, with the actuator subsystem at roughly $3,780. The QDD architecture choice, cheaper planetary gearboxes with bigger motors instead of expensive strainwave drives, is a genuine structural advantage. Unitree can iterate a new actuator design in weeks, not quarters. That’s not a marginal benefit. That’s a compounding one.

The piece nails the ecosystem point too. China’s 200+ humanoid companies are all feeding and drawing from the same component supply chain. Every province now has multiple manufacturers of gearboxes, motors, and encoders sized for humanoids. Unitree didn’t just build a robot, they helped catalyze an entire manufacturing ecosystem. That’s the BYD parallel working in real time.

The Margin Nuance: List Price vs. Realized Price

Here’s where we diverge, not on the BOM, but on what price you attach to it.

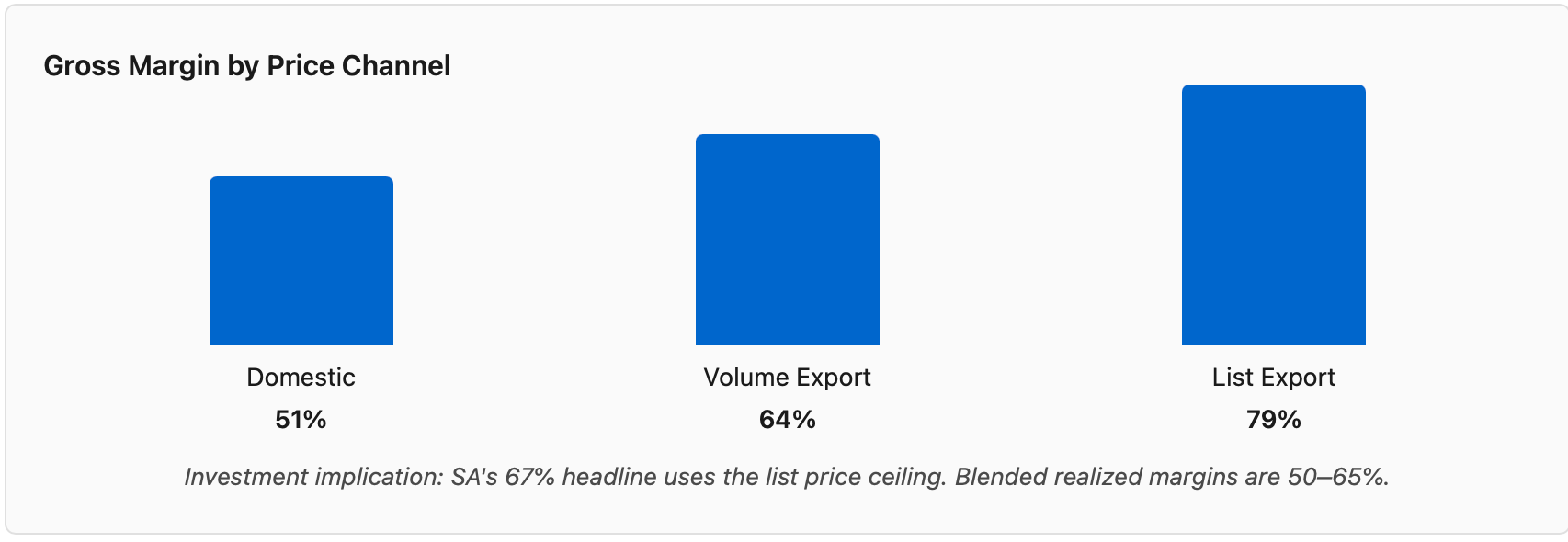

SemiAnalysis cites 67% gross margins on the G1. That number is real at their cited export list price of $27,300. That’s the ceiling, not the average. It’s like quoting Apple’s gross margin on the iPhone Pro Max and pretending every iPhone sells at that price.

Here’s the actual pricing structure:

Source: CNP Securities teardown, Unitree First Round Inquiry Response (SSE), industry channel checks.

The majority of Unitree’s volume ships domestically at ¥85,000, that’s approximately $11,700 at current exchange rates. CNP Securities’ own analysis puts margins at “exceeding 40%” at that domestic price, which our math confirms at roughly 51%. Export deals in volume, the ones actually closing, not the sticker price, land between $16,000 and $22,000. Blended across channels, we estimate realized gross margins of 50–65%.

That’s still exceptional. A 50–65% gross margin on a $5,700 BOM is the kind of unit economics most hardware companies dream of. But there’s a meaningful difference between 50% and 67% when you’re projecting out to market dominance. At 50%, you have less room to absorb warranty costs, service contracts, and the inevitable reliability fixes that come with early deployments. At 67%, you’re swimming in margin. SA used the ceiling. The average is lower.

This matters because Unitree’s entire pitch to the market, and the narrative around their IPO, hinges on margin sustainability. If the blended margin is 50–55% instead of 67%, the path to profitability on deployment-grade robots gets longer, not shorter.

The Actuator Cost SA Didn’t Break Down

SemiAnalysis correctly identifies actuators as 66% of the BOM. They don’t break down what’s inside. We will.

The G1 uses PMSM motors with harmonic reducers, not pure QDD that eliminates the gearbox entirely. SA’s piece uses “QDD” loosely to describe the architecture, but the G1’s joints still use harmonic drives in key locations. This is an important distinction because harmonic reducers are the most expensive single component in the actuator stack.

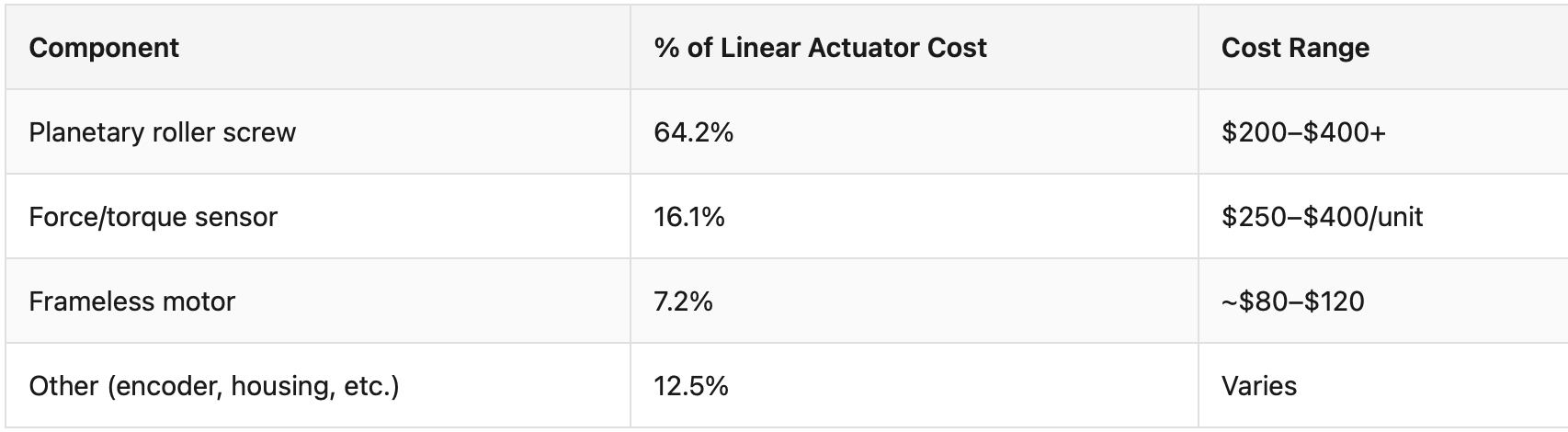

Here’s the cost structure of a typical linear actuator in the G1:

Source: CNP Securities teardown, component supplier pricing, industry contacts.

The planetary roller screw alone accounts for nearly two-thirds of the linear actuator cost. And a basic ball-screw runs $100 to $120 per unit. A planetary roller screw, higher precision, better load capacity, longer life, runs $200 to $400+. That delta is where Unitree’s cost advantage lives. They’re not using the cheapest possible components. They’re using mid-tier components at scale pricing, which is a different and more defensible position.

The force/torque sensors are another line item SA glossed over. At $250–$400 per unit, these are not commodity items. They’re precision instruments that measure contact forces in real time, and they’re critical for any robot that needs to interact with the physical world safely. Unitree sources these domestically, which keeps costs down, but the sensor market is consolidating. If a single supplier gains pricing power, as HarmonicDrive did in strainwave gearboxes for decades, Unitree’s BOM advantage narrows fast.

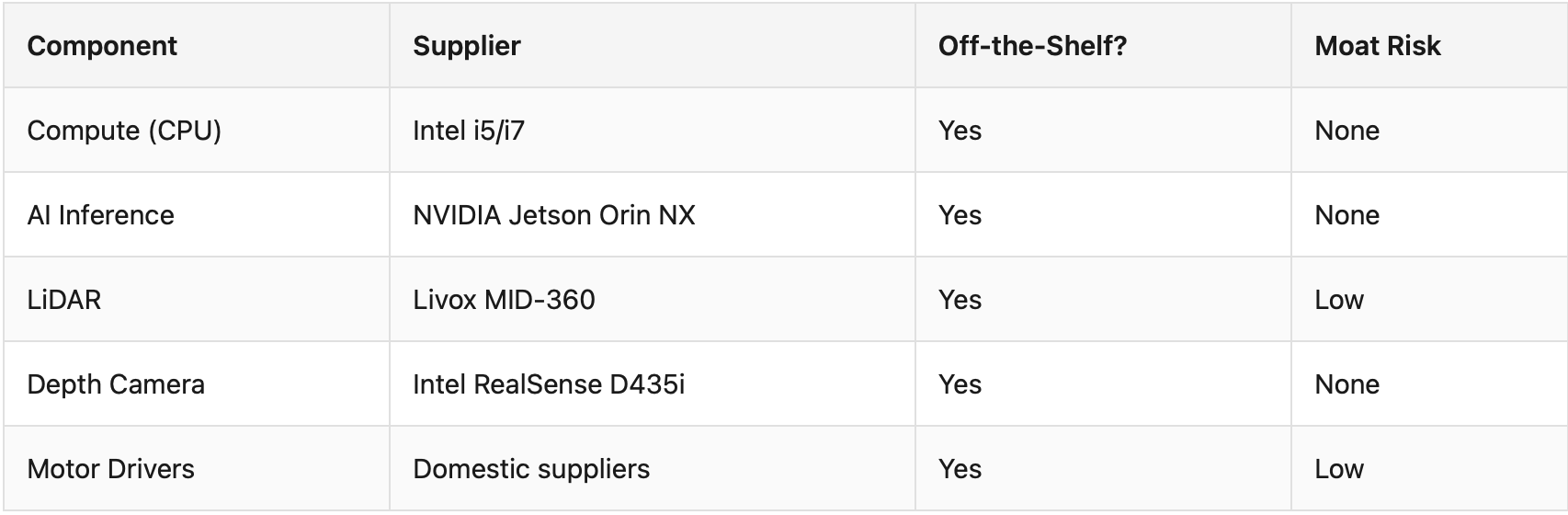

No Custom Silicon: Manufacturing Advantage, Not Technology Moat

“Every critical semiconductor in the G1 is commercially available. Any competitor with a purchasing department can buy the same compute, the same sensors, the same motor drivers.”

This is the point nobody in the Unitree hype cycle is talking about.

Every chip in the G1 is off-the-shelf. The compute stack runs Intel i5/i7 processors paired with NVIDIA Jetson Orin NX modules. The LiDAR is a Livox MID-360. The depth camera is an Intel RealSense D435i. There is no custom silicon. No Unitree-designed ASIC. No proprietary inference chip. Nothing.

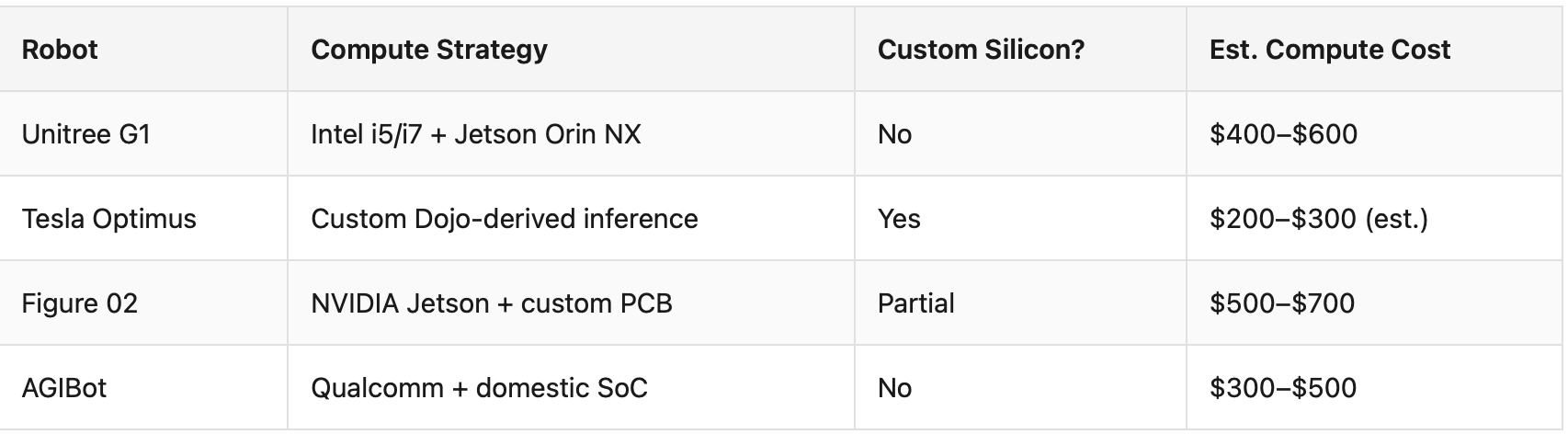

Compare that to Tesla Optimus, which is designing custom Dojo-derived inference silicon for its humanoid. Or to Apple, which has shipped custom silicon in every product category it enters. The companies that dominate hardware categories long-term almost always design their own chips. Unitree hasn’t done this.

Now, does it matter today? Not really. The commodity compute stack is cheaper, available at volume, and good enough for teleoperated and semi-autonomous tasks. But it means Unitree’s advantage is manufacturing and cost, not technology. Anyone with access to the same Chinese supply chain can build a robot with the same Intel + Jetson stack, the same Livox LiDAR, the same RealSense camera. The hardware is reproducible. The manufacturing process, the iteration speed, the supplier relationships, the vertical integration, is the moat. And manufacturing moats erode faster than technology moats.

There’s also a reliability implication. Consumer-grade compute components aren’t designed for continuous industrial duty cycles. That’s acceptable in a research lab. It’s a warranty nightmare in a warehouse running two shifts. SA mentions viability but doesn’t quantify what happens when a $5,700 robot needs a compute board swap after extended deployment.

Source: Teardown estimates, industry contacts, CNP Securities.

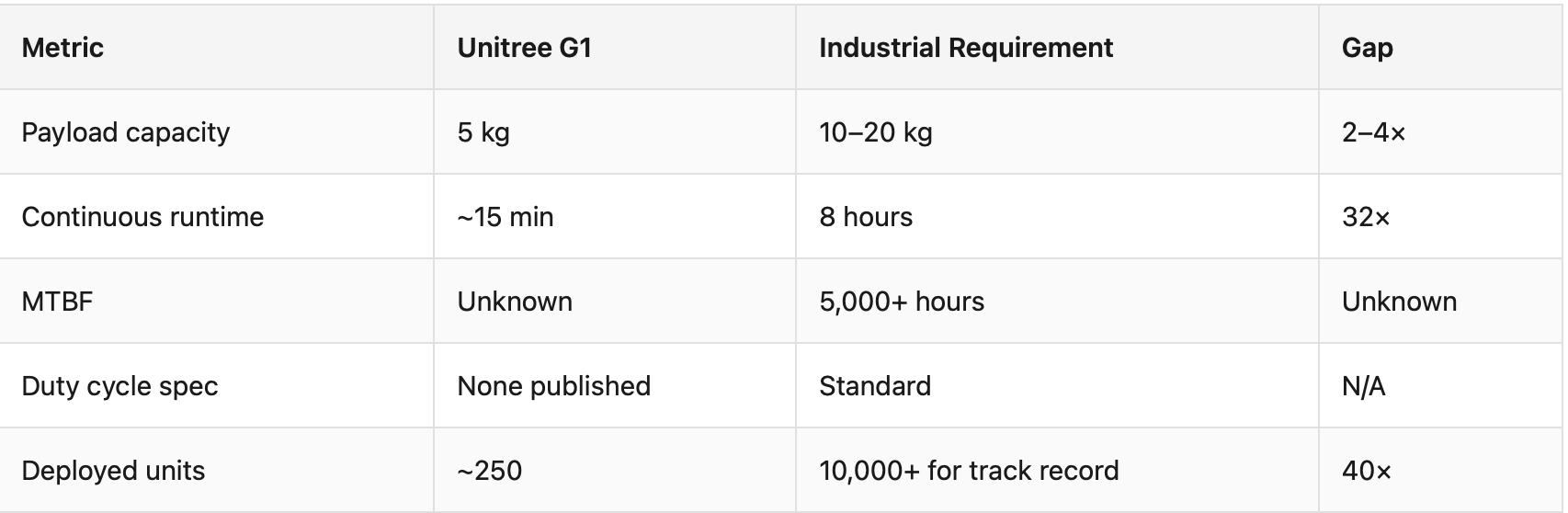

The Reliability Gap: 250 Units Is a Pilot, Not a Threshold

SemiAnalysis frames approximately 250 deployed G1 units as crossing a “viability threshold.” We’d frame it differently. Two hundred fifty units is a pilot program.

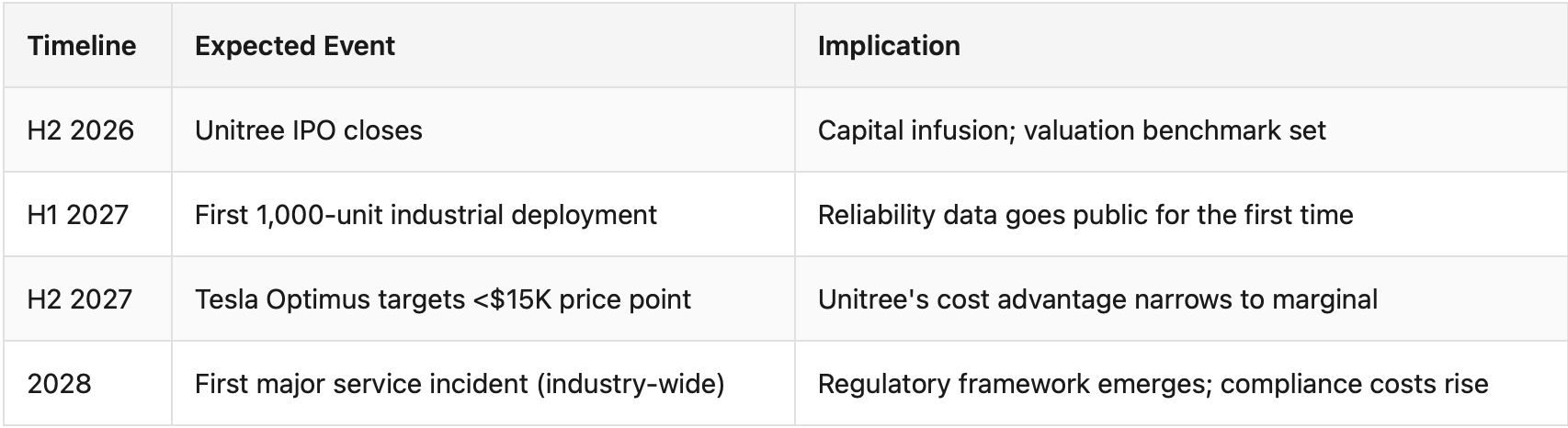

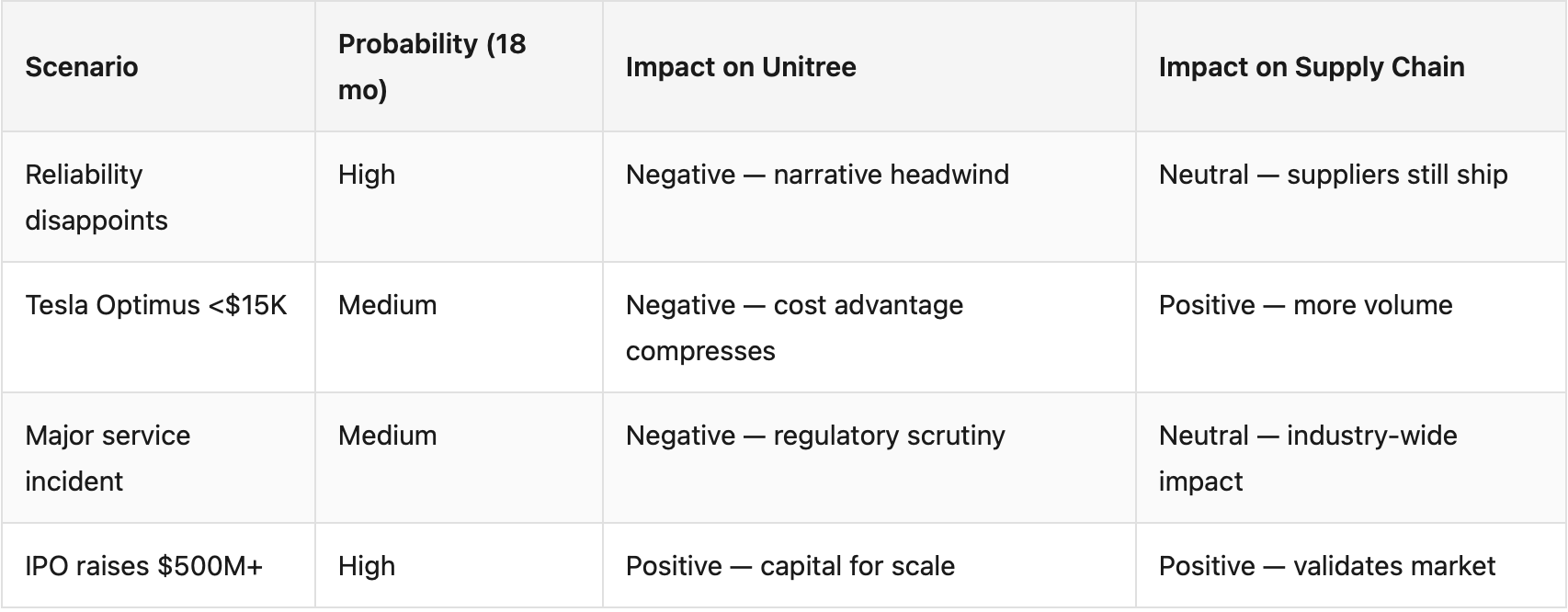

Forward risks (18 months):

Reliability data will surface failure modes that don’t show up in lab testing, narrative headwind for the “dominance” thesis.

Tesla Optimus may break $15,000 by 2027 with custom silicon and the same Chinese supply chain, compressing Unitree’s cost advantage from structural to marginal.

The first major service incident (property damage or injury) will trigger a regulatory and perception reckoning across the industry.

There is no published MTBF data for the G1. There are no duty cycle specifications. There are no long-term reliability studies. The robot carries 5 kg for 10–15 minutes before needing a cooldown. That's up from 2–3 minutes a year ago, impressive iteration, but it's not a factory floor number. A human warehouse worker handles 10–20 kg payloads for eight hours. The G1 handles 5 kg for 15 minutes with teleoperation.

The economic calculation SA presents, Unitree below $30/hour labor cost, assumes full teleoperation, a two-year useful life, zero residual value, and only two shifts. Those are conservative assumptions, and we respect the honesty. But “conservative assumptions” on a 250-unit deployment base is still a projection, not a track record. The first time a G1 drops a tote on a warehouse floor and damages $50,000 of product, or the first time a unit fails mid-shift and halts a conveyor line, those economics change overnight.

We’re not saying it won’t work. We’re saying the data doesn’t exist yet to prove it does. Two hundred fifty deployed units across multiple customers with no published uptime data is a proof of concept. BYD shipped 189,000 EVs in 2020 before the market took them seriously. Unitree has shipped 5,500+ G1 humanoids through 2024–2025. The scale difference is an order of magnitude.

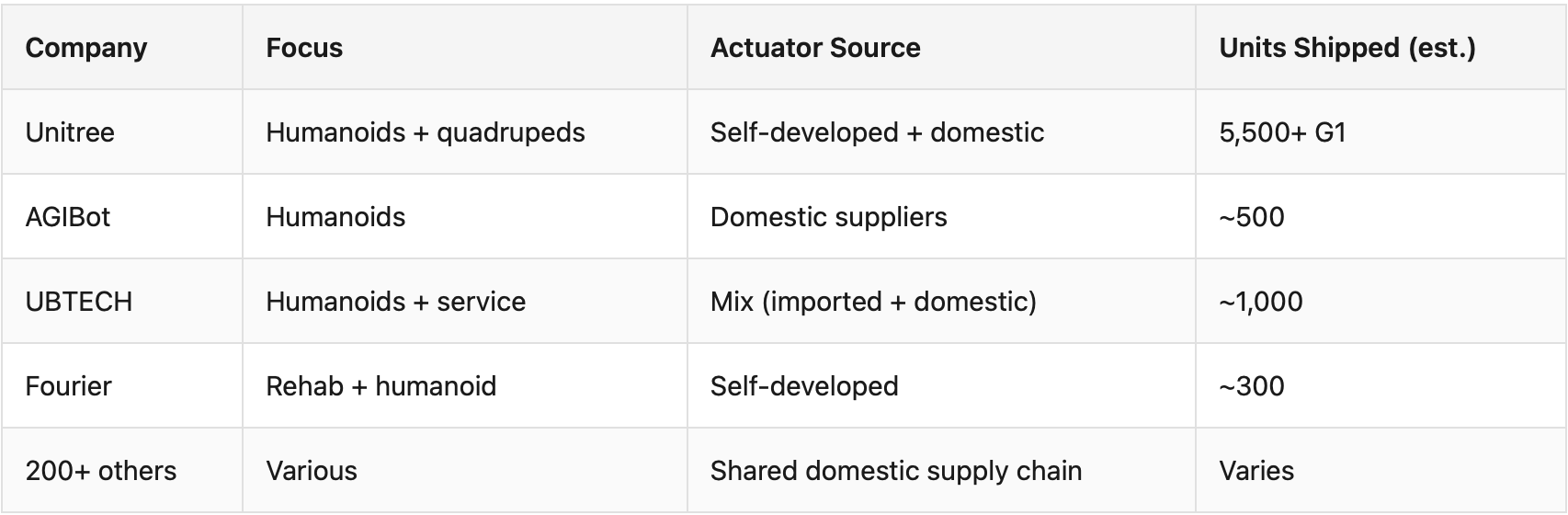

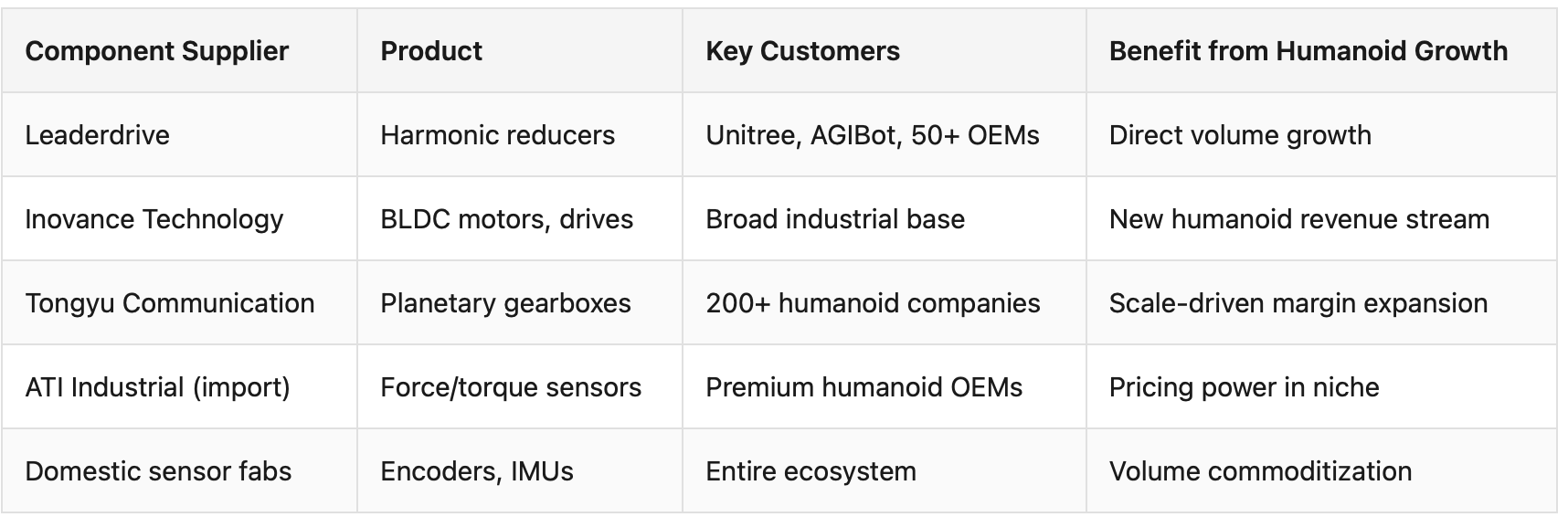

The Real Winner: China’s Actuator Supply Chain

The picks-and-shovels play: Harmonic drive manufacturers, frameless motor specialists, and sensor fabs in Shenzhen and Suzhou are the real winners. They sell to every humanoid OEM, Chinese or Western. The component supply chain captures value regardless of which humanoid wins.

Here’s the part of the story SA touched on but didn’t fully develop, and it’s the most important investment thesis in the piece.

There are over 200 humanoid robot companies in China right now. Every one of them needs actuators. Every one of them needs gearboxes, motors, encoders, and sensors. And the supply chain that Unitree helped build is now available to all of them.

Source: Industry estimates, company filings, CNP Securities.

This is the real BYD parallel. BYD’s battery cell strategy created an ecosystem of suppliers, Hunan Yuneng, Shenzhen Dynanonic, Inovance, Sanhua, that now supply the entire Chinese EV industry. BYD won, but so did the component suppliers. The same dynamic is playing out in humanoids.

Companies like Leaderdrive (harmonic reducers), Inovance (motors), and the dozens of planetary gearbox manufacturers now shipping at volume, these are the picks and shovels of the humanoid gold rush. They win whether Unitree dominates or whether AGIBot, UBTECH, Fourier, or any of the other 200+ companies takes the crown.

Unitree’s verticalization is impressive. They self-develop BLDC motors, planetary gearboxes, LiDARs, and depth cameras. Their S-1 filing explicitly states that scaling production gave them upstream bargaining power, which translated to quadruped margins improving from 42.36% to 55.49% while costs dropped nearly in half. But even Unitree sources from the broader ecosystem. And that ecosystem is commoditizing fast.

Source: Industry contacts, CNP Securities, company filings.

If you’re looking for the investment thesis buried in SA’s piece, it’s not “buy Unitree.” It’s “watch the component suppliers.” The actuator supply chain is the infrastructure layer, and infrastructure layers capture value regardless of which application-layer company wins.

What Comes Next

Unitree’s upcoming IPO is a milestone, not a turning point. BYD’s IPO didn’t make it dominant, a decade of iteration did. DJI never needed to go public at all. An IPO gives Unitree capital to scale manufacturing and fund R&D. It doesn’t solve the reliability question or the margin question.

We expect three things in the next 18 months:

First, reliability data will disappoint. Not because the robots are bad, but because the expectations are too high. When you’re selling a $5,700 robot into industrial environments with consumer-grade compute and no published MTBF, early deployments will surface failure modes that don’t show up in lab testing. This is normal. Every hardware company goes through it. But it will create a narrative headwind for the “dominance” thesis.

Second, Tesla Optimus will break the $15,000 price barrier by 2027. Tesla has the same Chinese supply chain access, a larger engineering team, and custom silicon in the pipeline. If Optimus hits $15,000 with better reliability and Tesla’s brand in industrial sales, Unitree’s cost advantage compresses from structural to marginal.

Third, the first major service incident will reset expectations. When a humanoid robot causes property damage or injury in a commercial deployment, and it’s a matter of when, not if, the entire industry will face a regulatory and perception reckoning. Unitree, as the highest-volume player, will be first in the crosshairs.

Bottom Line

SemiAnalysis wrote the definitive overview of Unitree’s strategy, cost structure, and market position. The BYD/DJI analogy is tight. The BOM teardown is accurate. The ecosystem analysis is thorough. It’s a strong piece.

But “will dominate global robotics” is a timeline call, and the timeline is longer than the piece suggests. Unitree’s 50–65% blended margins are real but lower than the 67% headline. Their 250 deployed units are a pilot, not a threshold. Their lack of custom silicon means the moat is manufacturing, not technology. And 200+ Chinese competitors are drawing from the same supply chain that Unitree helped build.

The cost advantage is real. The strategy is sound. The BYD/DJI playbook is the right one. But dominance requires reliability data that doesn’t exist yet, and the deeper play, the one that doesn’t depend on which humanoid wins, is the component supply chain.

Watch the actuators. Watch the sensor suppliers. Watch the gearbox manufacturers. They’re building the infrastructure layer of humanoid robotics, and they win regardless of whether Unitree’s G1 becomes the iPhone or the Galaxy of this market. That’s the thesis worth betting on.