Sensors Part 1: The $168M Nobody Sees

A rounding error in the robotics world. Until you do the math.

The Sensor Nobody Covers · Part 1 of 4

In 2008, the entire lithium-ion battery market for electric vehicles was worth about $400 million. Four hundred million dollars. Toyota was selling more Priuses in a quarter than the entire global EV battery industry was generating in revenue. If you went to a sell-side conference and pitched lithium-ion batteries as an investment theme, people looked at you like you were trying to sell them swampland.

Ten years later, that market was $44 billion. The companies that positioned early (Panasonic, CATL, LG Chem) became the backbone of the largest industrial transition since the internal combustion engine replaced the horse. Panasonic locked in its supply deal with Tesla. CATL rode the Chinese EV boom to become the world’s largest battery manufacturer. LG Chem spun off its battery division into a standalone company worth more than the parent. The early movers didn’t just participate in the growth. They defined it.

I think about that pattern a lot. The market is invisible, then it’s inevitable. And right now, I’ve found another one.

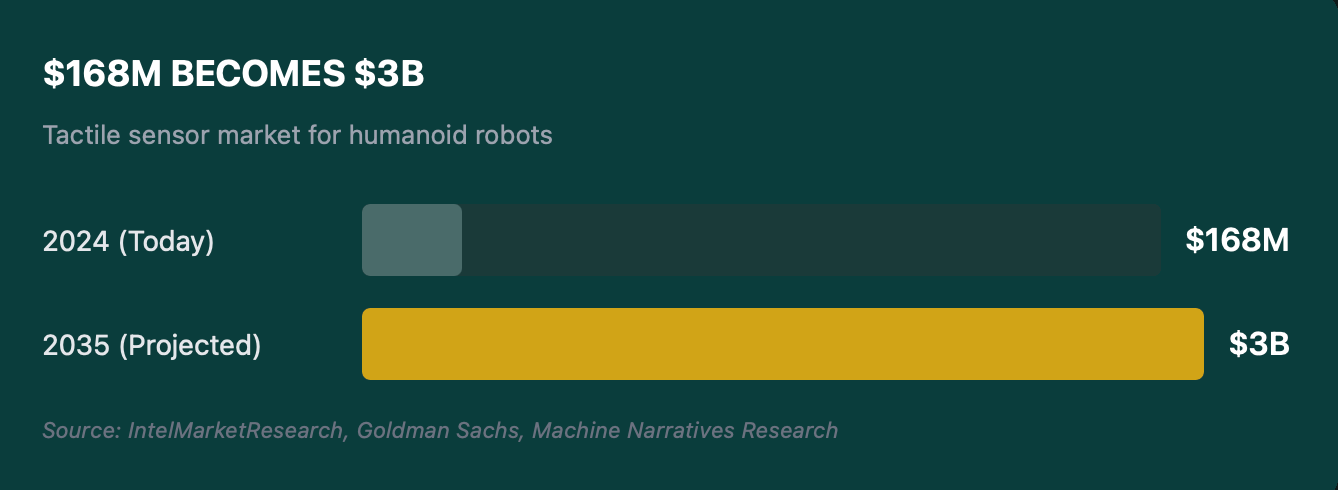

$168 million. That’s the entire global market for tactile sensors in humanoid robots. I had to read the number twice. I’ve been covering robotics and semiconductor supply chains for years, and I’d never seen this figure before. Not because it’s new. Because nobody thought it was worth tracking.

Let me explain why I think that’s about to change.

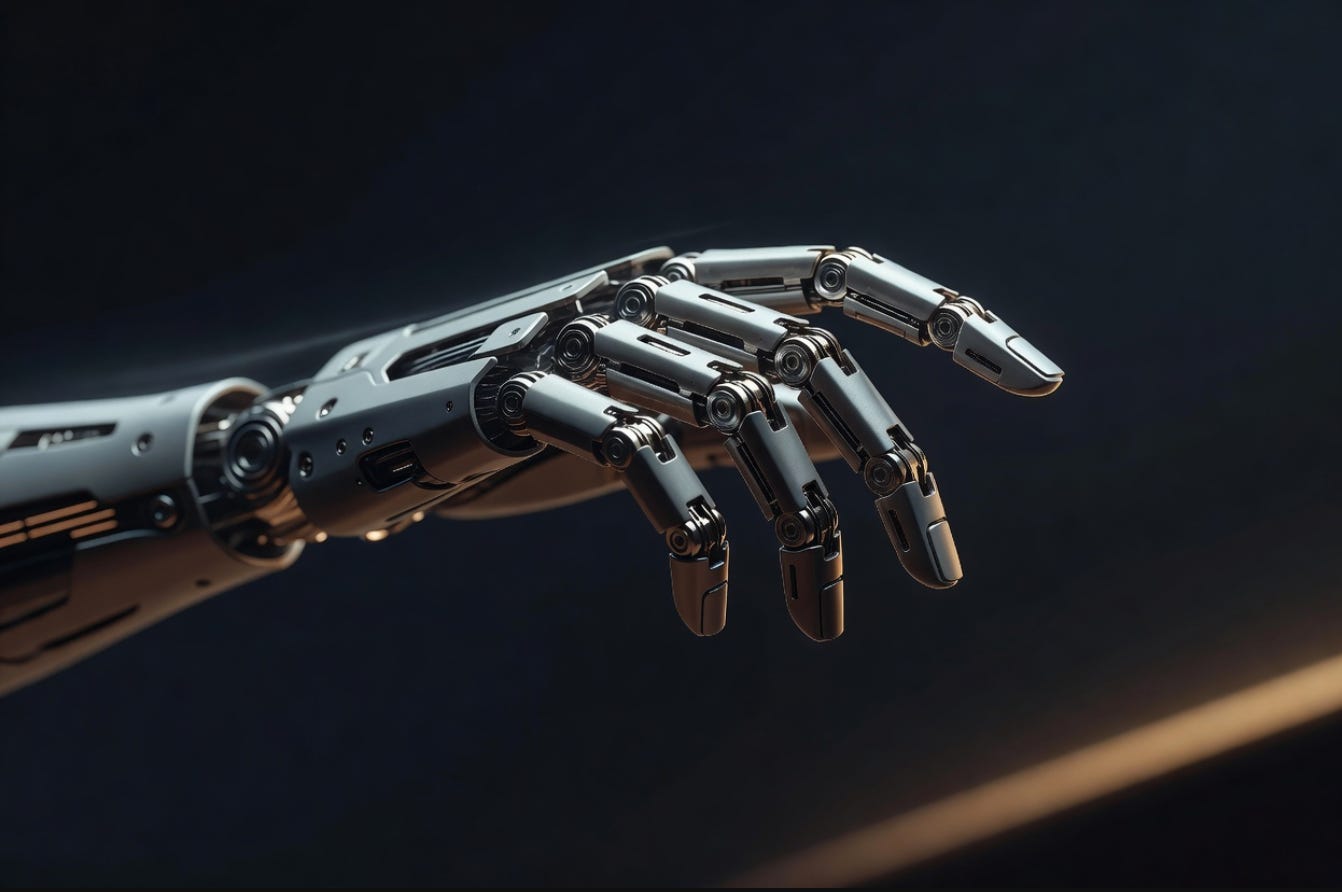

A tactile force/torque sensor, smaller than a fingertip, that enables robotic touch perception.

The Number That Caught My Eye

$168 million. That’s the total addressable market for tactile sensors in humanoid robots, according to IntelMarketResearch’s 2026 report. To put that in perspective, Novanta paid $172 million to acquire ATI Industrial Automation (a single sensor company) in 2021. The entire global market for these sensors is worth less than one acquisition from five years ago.

$172 million. That’s what Novanta paid to acquire ATI Industrial Automation — a single sensor company — in 2021. The entire global market for tactile sensors in humanoid robots is worth $168 million. One acquisition cost more than the whole market.

It wouldn’t cover the quarterly R&D budget of a mid-tier automaker. It wouldn’t register on the radar of a thematic ETF manager. It’s the kind of number that gets buried on page 47 of an industry report that maybe three people read, and two of them work at the company that wrote it.

I didn’t stumble across this number through some brilliant research process. I found it because I was trying to build a bill-of-materials model for humanoid robots. Trying to understand what actually goes into these things, component by component. I kept getting stuck on the sensing layer.

The actuator numbers are well-documented. Motor specs, gear ratios, torque curves: all published. The compute costs are public. Nvidia’s Jetson pricing, Qualcomm’s robotics chips, the cost per TOPS: you can look it all up. But when I tried to find the sensor data, I ran into a wall. Nobody was aggregating it. Nobody was tracking the demand curve. The data existed, fragmented across a dozen research reports that don’t talk to each other, and nobody had pulled it together.

When I finally got the number, I thought it was wrong. A hundred and sixty-eight million dollars? For the sensors that give robots the sense of touch? For the technology that’s supposed to make humanoid manipulation viable? It seemed absurd.

Then I started to understand why it’s so small, and that’s when it got interesting.

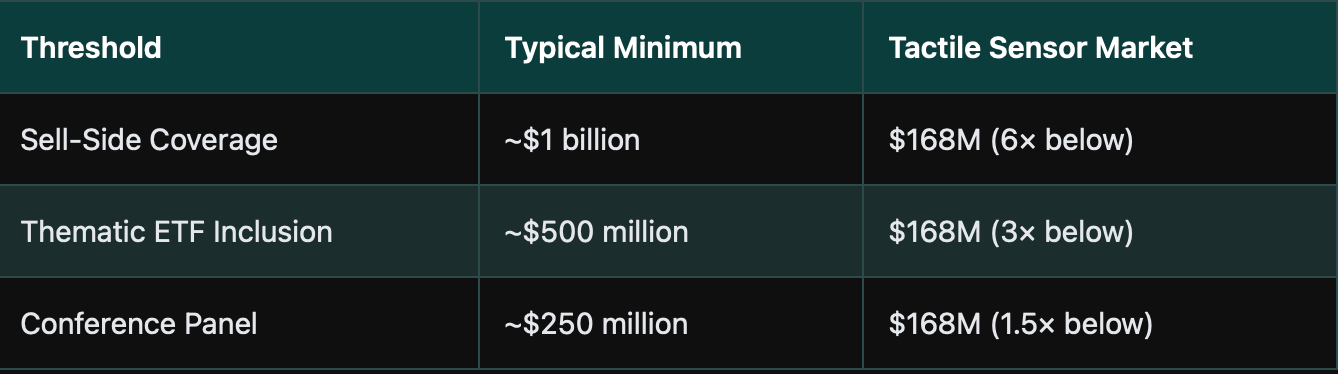

The market is too niche for ETFs. It’s too small for sell-side coverage. It’s too early for earnings calls. The institutional world has a blind spot for markets under $1 billion: no model, no coverage, no analyst who wakes up thinking about tactile sensor procurement for humanoid robots. The companies making these sensors are small, mostly private, and operating at production volumes that would be dwarfed by a single large humanoid manufacturer’s annual needs.

That’s not a gap. That’s a blind spot. And blind spots are where alpha lives.

The Goldman Sachs Math

Then I found the projection that changed my mind.

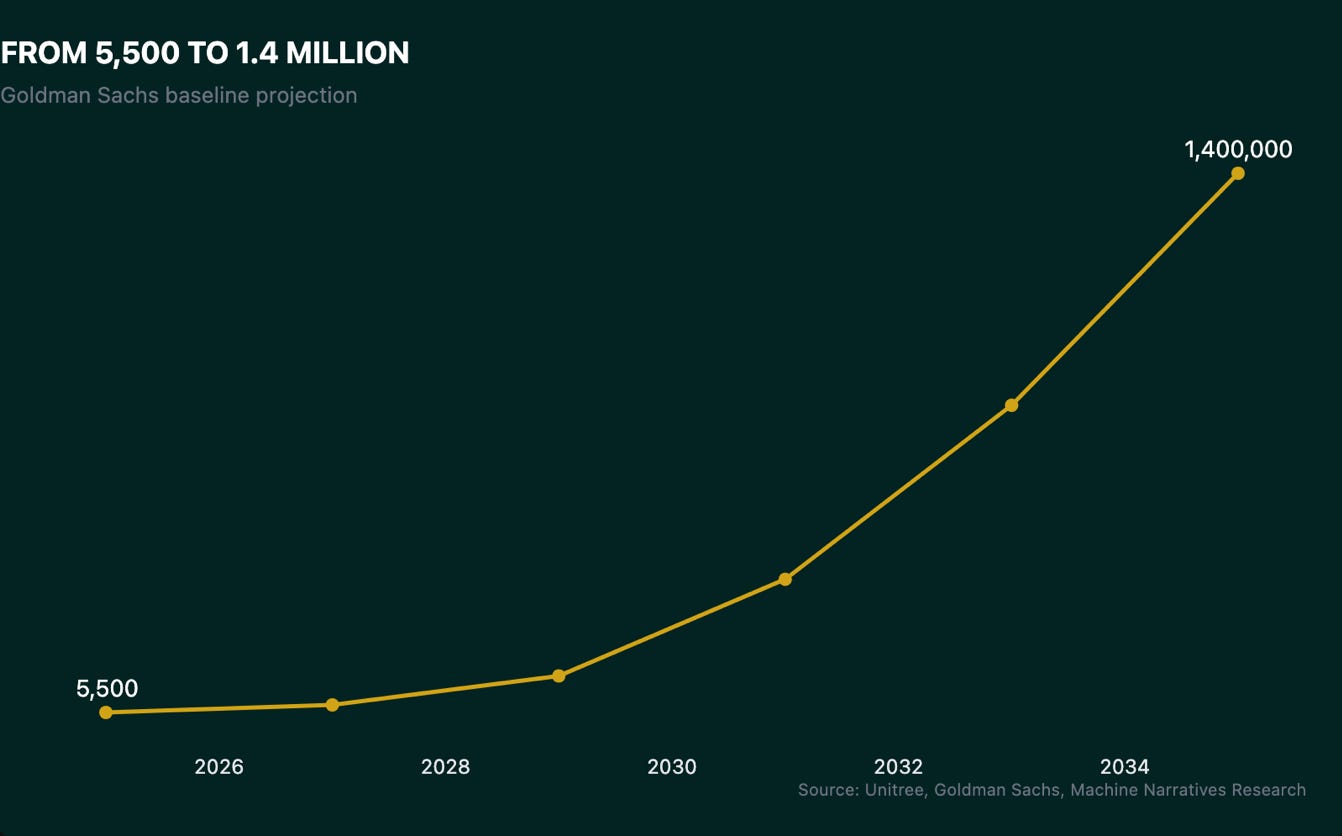

Goldman Sachs projects 1.4 million humanoid robot shipments by 2035. That number alone is worth pausing on. 1.4 million humanoid robots, shipped and deployed, in just over a decade. But the number that made me sit up was what happens to the sensor market when you multiply it out.

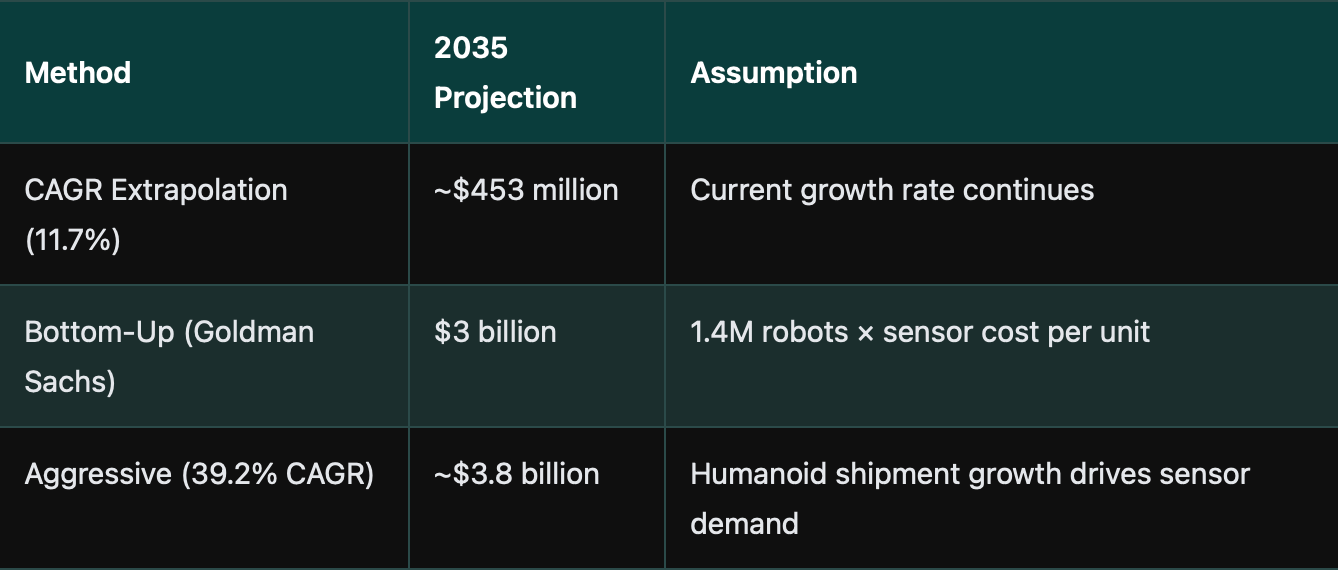

$168 million becomes $3 billion.

I checked the math three times because I didn’t believe it. Let me walk through it so you can check it too.

The $3 billion figure isn’t a CAGR extrapolation. I want to be clear about that, because the two methods get confused constantly in market reports. A simple CAGR extrapolation of 11.7% over nine years would only get you to about $405 million. That’s meaningful growth, but it’s not the story.

The $3 billion comes from a bottom-up calculation: Goldman’s 1.4 million robot shipments by 2035, multiplied by the estimated sensor cost per robot. Each humanoid robot needs both force/torque sensors and tactile sensors. Force/torque sensors (the ones that measure load at wrists, ankles, and knees) are the mature market, roughly $2.3 billion globally and growing at about 6% annually. But tactile sensors (the ones that give a robot the ability to feel pressure distribution, texture, and slip) are where the exponential part kicks in.

When you scale from a few thousand prototype units to 1.4 million production units, the per-unit costs drop, the supply chains mature, and the total addressable market transforms. That’s the transition from lab curiosity to industrial commodity. I’ve seen this movie before. In lithium-ion batteries. In MEMS accelerometers. In CMOS image sensors. The pattern is always the same: the market looks too small to matter until it doesn’t.

And here’s the part that should make you pay attention: the Goldman baseline was set before Tesla committed $25 billion to AI and robotics for 2026. Before Unitree shipped 5,500 humanoid units in 2025 (the only verified mass-production data point we have). Before Figure AI started talking about production runs, not prototypes. The baseline was modeled when humanoids were still lab curiosities. The world has moved since then. Nobody revised the number.

Some forecasters use 39.2% CAGR for humanoid robot shipments, which would blow past the $3 billion figure well before 2035. I don’t know which number is right. But I think the direction is right, and in markets this early, direction matters more than precision.

Why Nobody’s Watching

I want to spend a minute on the institutional dynamics here, because I think they matter.

The reason nobody’s watching this market is structural. A $168 million market doesn’t clear the threshold for dedicated sell-side coverage. You can’t build a career on it. You can’t justify a conference panel. It doesn’t show up in anyone’s thematic ETF because the underlying companies are too small or too private. The sensor companies themselves are part of the invisibility problem: they’re small, they’re fragmented, and they’re not the kind of names that generate clicks.

Every institutional framework for evaluating robotics focuses on the same three things: actuators, AI, and compute. Those are the big-ticket items, the ones with billion-dollar markets and established supply chains. Sensors are a footnote. The bill of materials for a humanoid robot gets broken down into motors, batteries, controllers, and maybe “sensing systems” as a line item. Nobody drills into the sensing layer. Nobody aggregates the demand curve for tactile sensors across projected humanoid production.

Here’s what the career math looks like. A junior analyst at a major bank pitches their desk head on covering tactile sensors for humanoid robots. The desk head asks: “How big is the market?” The analyst says $168 million. The meeting lasts another thirty seconds. You can’t justify a headcount, a conference slot, or a morning note on a market that small. The analyst who writes that report is betting their career on a niche nobody at the firm has ever mentioned in an earnings preview. So nobody writes it. And the blind spot persists.

Think about what that means at scale. Every major bank, every asset manager, every research house runs the same calculus. The market is too small to cover, so nobody covers it. Because nobody covers it, the institutional world doesn’t know it exists. Because the institutional world doesn’t know it exists, nobody allocates to it. The feedback loop is self-reinforcing. The blind spot isn’t just structural. It’s stable.

The alpha isn’t in knowing something nobody else knows. It’s in paying attention to something nobody else thinks is worth paying attention to.

I’d argue this is the most important observation here. And the institutional incentive structure makes it almost impossible for anyone to be the first mover on this.

But the demand curve doesn’t care about institutional incentive structures. It just is.

The Timing

What makes this different from other small markets is the convergence of signals.

Tesla’s $25 billion commitment to AI and robotics in 2026 is not a research budget. It’s a production budget. That’s the kind of money you spend when you’re building factories, not prototypes. When the largest EV manufacturer in the world commits that kind of capital to humanoid robots, the supply chain implications ripple outward. Every component supplier in the chain gets pulled along.

Unitree shipped 5,500 humanoid units in 2025. Real units, shipped to real customers, with real sensors inside them. Not a press release about a prototype. That volume is small relative to the $3 billion projection, but it’s the first verified data point that humanoid production is real, not theoretical.

Figure AI is raising at a $39 billion valuation. Boston Dynamics switched from hydraulic to electric Atlas specifically to optimize for manufacturing. Agility Robotics signed a deal with Amazon for warehouse deployment. 1X Technologies is scaling its NEO line for home assistance. Sanctuary AI is targeting general-purpose labor. The list of companies making production bets, not science experiments, is growing every quarter.

The demand curve isn’t theoretical anymore. It’s happening. The question isn’t whether humanoid robots will ship in meaningful quantities. The question is how fast, and who supplies the components.

In the next article, we’ll show the engineering challenge — the touch gap between human and robot sensing. Your fingertip has 2,500 receptors per square centimeter. The best commercial tactile sensor has 12. That gap is real, and it’s expensive. But first, let’s talk about what that gap means for the market.

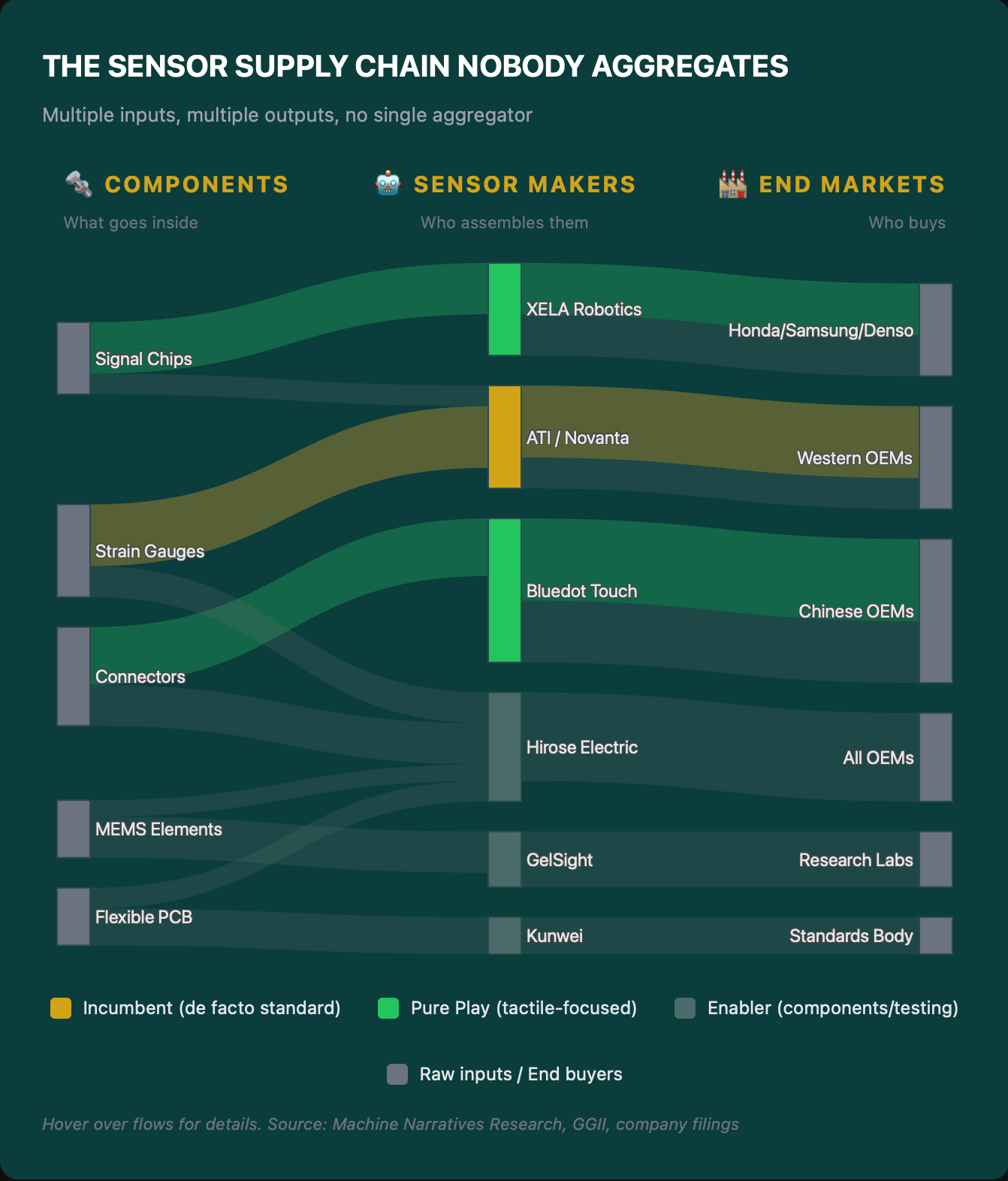

The sensor landscape is fragmented in a way that makes aggregation almost impossible. No single report pulls these names together. No ETF holds them. No sell-side model tracks the demand curve across projected humanoid production. Let me walk you through why.

The Incumbent

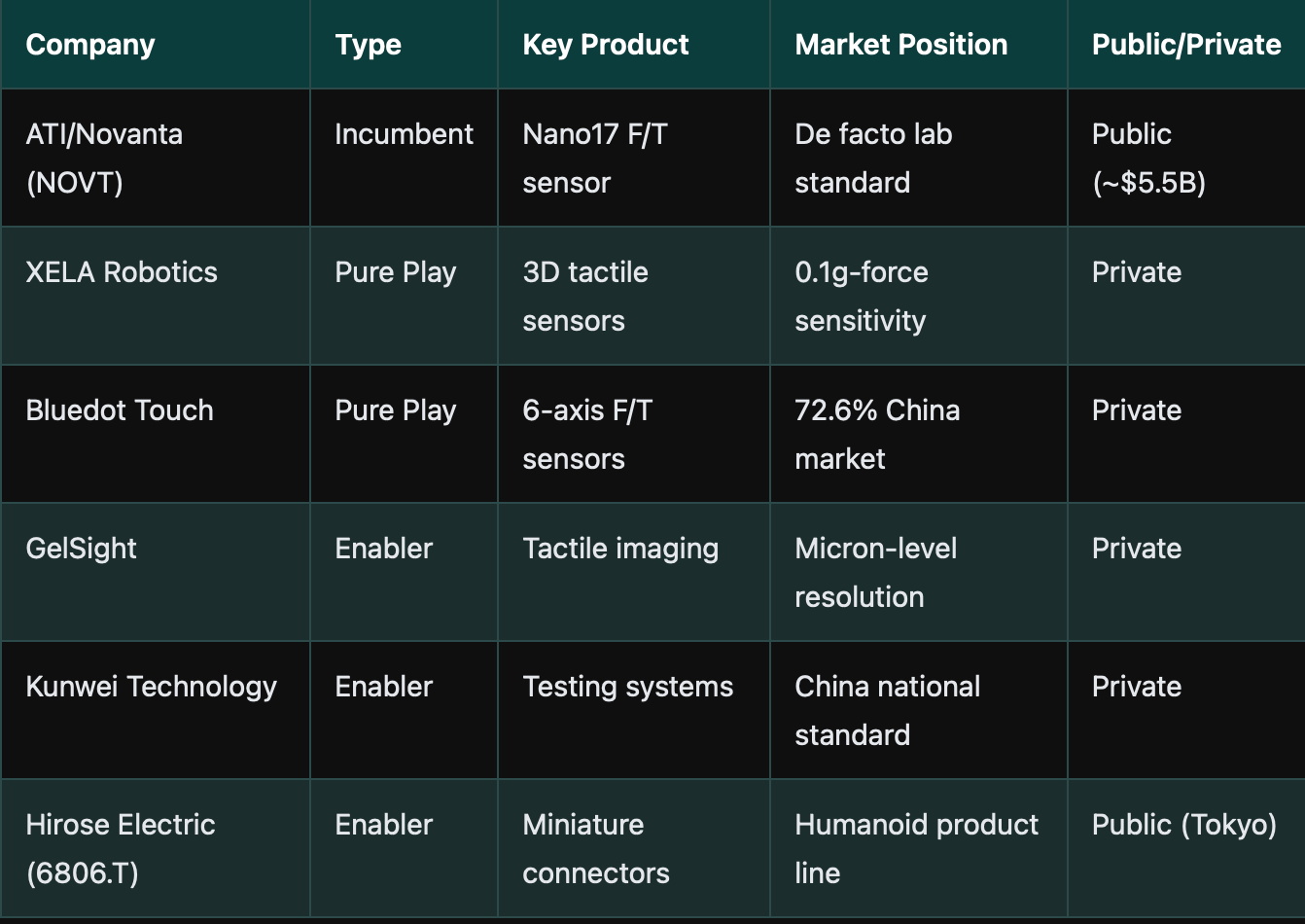

ATI Industrial Automation’s Nano17 is the de facto standard in every major robotics lab worldwide. Seventeen millimeters in diameter, 9 grams. If you’re doing force/torque research on a humanoid robot, you’re probably using an ATI sensor. Novanta (NOVT) acquired them for $172 million in 2021. At the time, that looked like a niche tuck-in. In hindsight, it might be the most prescient sensor acquisition of the decade.

Novanta’s market cap is around $5.5 billion today. ATI is a meaningful piece of their revenue mix, and if the tactile sensing wave drives demand for integrated force/torque plus tactile sensing across humanoid joints, Novanta benefits from the volume increase. It’s not pure-play, but it’s real revenue from real sensors on real robots. And the acquisition price tells you what Novanta’s leadership thought was coming. $172 million for a sensor company in 2021, before anyone was talking about humanoid production at scale. That’s conviction.

The Pure Plays

XELA Robotics, out of Tokyo and Taipei, makes 3D tactile sensors that detect forces as light as 0.1 gram-force. That’s roughly the weight of a mosquito landing on skin. Their customer list reads like a who’s who of robotics: Honda, Hitachi, Samsung, Denso, Sanctuary AI. Private, which means no direct public play. But they’re the name that comes up first in every conversation about tactile sensing.

Bluedot Touch controls 72.6% of the Chinese humanoid robot force/torque sensor market, per a 2025 GGII report. China is building its own humanoid supply chain deliberately, with government backing, and Bluedot is sitting at the center of it. Kunwei Technology drafted China’s national standard for robot sensor testing. When a company writes the standard, it tells you something about its position in the ecosystem. Both are private. Both are names that surface when you dig into the Chinese robotics supply chain. The fact that China has dedicated sensor companies writing national standards tells you how seriously Beijing takes the humanoid buildout.

The Enablers

GelSight makes high-resolution tactile imaging sensors: the kind that can map surface texture at micron-level resolution. SynTouch developed BioTac, a biomimetic tactile sensor that mimics the human fingertip. The company dissolved in 2024, but the technology set the standard for biomimetic sensing in research labs worldwide. Both names surface in every serious conversation about robotic touch.

And then there’s the connector and flexible circuit layer. Hirose Electric (6806.T) is developing miniature connectors and flexible printed circuits specifically for humanoid wiring harnesses. When a major connector company builds an entire product line around a single application, that tells you how serious the demand signal is. Hirose isn’t a sensor company. They’re an infrastructure company betting that humanoid robots will need a wiring architecture that doesn’t exist yet.

The problem is aggregation. These companies don’t show up together in anyone’s model. There’s no ETF, no index, no sell-side report that pulls together the demand curve for tactile sensors across projected humanoid production. The data exists, fragmented across a dozen research reports. But nobody’s built the composite picture.

I want to remind readers: the most cited number ($168 million) comes from a single report by IntelMarketResearch. No major research firm has published a comparable dedicated forecast for tactile sensors in humanoid robots. The methodology is somewhat opaque, and the definitional boundaries between tactile sensors, electronic skin, and haptic feedback are fuzzy: market researchers draw them differently. Hold the number loosely. But hold the direction tightly.

The Bear Case (Steelmanned)

Let’s steelman the counter arguments first, because that’s the right thing to do.

The bear case is straightforward. Humanoid robots are still mostly prototypes. Battery life is 2 to 4 hours. AI perception is immature. Dexterous manipulation is limited. Costs range from $50,000 to $250,000 per unit. If humanoid production stays niche (if these remain expensive toys for research labs and tech demos) the sensor market stays small. Not $3 billion. Maybe $400 million, which is what you’d get from a simple CAGR extrapolation of the current $168 million at 11.7% over nine years.

That’s still meaningful growth. But it’s not the kind that creates new market leaders or reshapes supply chains.

$400 million to $3 billion. Same market, two completely different stories. The bear case (CAGR extrapolation) says $400M. The bull case (bottom-up demand) says $3B. The direction is right either way.

For the bear case to hold, you need all of the following to be true simultaneously: Tesla’s $25 billion commitment doesn’t translate to production volume. Unitree’s 5,500 units in 2025 turns out to be a one-off. Boston Dynamics’ manufacturing pivot fails. Figure AI’s $39 billion valuation collapses. Every single production signal has to be wrong at the same time. Possible, sure. Probable? I don’t think so.

I think the bear case is plausible. I also think it’s wrong, and here’s why.

Tesla isn’t running a research lab. They’re building a factory. Unitree isn’t making prototypes. They’re shipping units. Boston Dynamics switched from hydraulic to electric Atlas specifically to optimize for manufacturing economics. These are production bets, not science experiments. The capital allocation tells you more than any market research report. When the largest companies in the world are committing billions to humanoid production, the demand curve for components follows.

The question isn’t whether demand for humanoid robot sensors will grow. It will. The question is whether it grows at 11.7% or 39% or something in between. And that range of outcomes is enormous for whoever positions early.

What I’m Watching

I’m not telling you to buy anything today. This market is too small, too fragmented, and too early for that kind of call. The companies closest to the tactile sensor opportunity (XELA, GelSight, SynTouch) are all private. The closest public proxy is Novanta, through ATI, and at a $5.5 billion market cap, it’s priced for steady growth, not explosive upside. The sensor demand curve could change that math, but it’s not a trade I’d make on a $168 million market.

What I am telling you is to watch this market. The companies that are positioned now (the ones with the sensor technology, the customer relationships, the production experience) will be the ones that benefit when the institutional world catches up.

When that first sell-side note drops, and it will, the analyst who writes it won’t be early. They’ll be late. The demand curve will already be established. The supply chain relationships will already be locked. The companies that got there first will have a significant advantage, and the coverage will read like a confirmation of what the market already priced in six months prior.

I’ve seen this pattern before. In lithium-ion batteries in 2008. In MEMS sensors in the early 2010s. In advanced packaging before CoWoS became a buzzword. The market is invisible, then it’s inevitable. The only question is how long the window stays open.

The first-mover advantage goes to whoever understands the demand curve before the sell-side catches up. And the sell-side isn’t even close.

Part 3 goes into the geopolitical risk: the supply chain chokepoints that could accelerate or constrain this market. If you think the sensor blind spot is interesting, wait until you see who controls the materials inside the sensors.

Anyways. That’s what I’m watching. Hope everyone has a great day, and I’ll talk to you soon.

This is Part 1 of The Sensor Nobody Covers. Part 2 shows the engineering challenge: the touch gap between human and robot sensing. Part 3 reveals the geopolitical risk: the supply chain chokepoints that could make or break this market. Part 4 goes deeper than anyone else is going.

Frequently Asked Questions

What happens to the sensor market if humanoid robots don’t scale?

If production stays niche at 10,000–20,000 units per year, the sensor market probably grows to $300–400M by 2035 via CAGR alone. That’s still meaningful growth, but it doesn’t create new market leaders or reshape supply chains. The $3B number requires volume production. If the robots don’t ship, the sensors don’t sell. The bear case isn’t zero — it’s just slow.

Why should I trust a market projection from a single research report?

You shouldn’t — at least not the exact number. The $168M comes from IntelMarketResearch, and no major research firm has published a comparable forecast. The definitional boundaries between tactile sensors, electronic skin, and haptic feedback are fuzzy. Hold the number loosely. But hold the direction tightly. Multiple independent data points (Goldman’s robot projections, company filings, production data) all point the same way.

What about sensors for industrial robots and cobots, not just humanoids?

The broader force/torque sensor market is about $2.3 billion globally, growing at 6% annually. That market is real, established, and covered by analysts. The humanoid-specific opportunity is what’s invisible. If you’re interested in the broader market, ATI/Novanta and Kistler are the established players. If you’re interested in the alpha, you’re looking at the humanoid-specific demand curve that nobody’s modeling.

How do I actually track this market as it develops?

Watch three things. First, humanoid robot shipment numbers — Unitree, Tesla, Figure AI quarterly updates. Second, GGII and IntelMarketResearch reports on sensor market sizing. Third, earnings calls — when an analyst asks Tesla’s CFO about force/torque sensor procurement, that’s the signal that institutional coverage has arrived. We’re not there yet.

The Sensor Nobody Covers: A 4-Part Series

Part 1: The $168M Nobody Sees (this article)

Part 2: The Touch Gap

Part 3: The Second Chokepoint

Part 4: What’s Inside the Sensor