Part 3: The 250% Tax: China’s Magnet Monopoly and the Robot Supply Chain It Could Choke

One country controls 94% of the magnets every robot needs. And they’ve already shown they’re willing to cut off supply.

NdFeB Supply Chain for Humanoid Robotics · Part 3 of 4

China produces 94% of the world’s sintered NdFeB magnets. Not 60%. Not 75%. Ninety-four percent. These are the magnets that make every servo motor in every humanoid robot on the planet spin. And on April 4, 2025, Beijing proved it was willing to weaponize that dominance — overnight, with zero warning, in retaliation for tariffs.

Export volumes plunged 74.3% year-over-year. European rare earth prices spiked to 6x Chinese domestic levels. Ford temporarily idled EV production lines. Elon Musk went on an earnings call and told the world that Tesla’s Optimus robot would need a Chinese export license to ship anywhere with magnets inside.

This is not a hypothetical supply chain risk. It already happened. The only question is whether it happens again — and what it means for the dozens of humanoid robotics companies that need these magnets to exist.

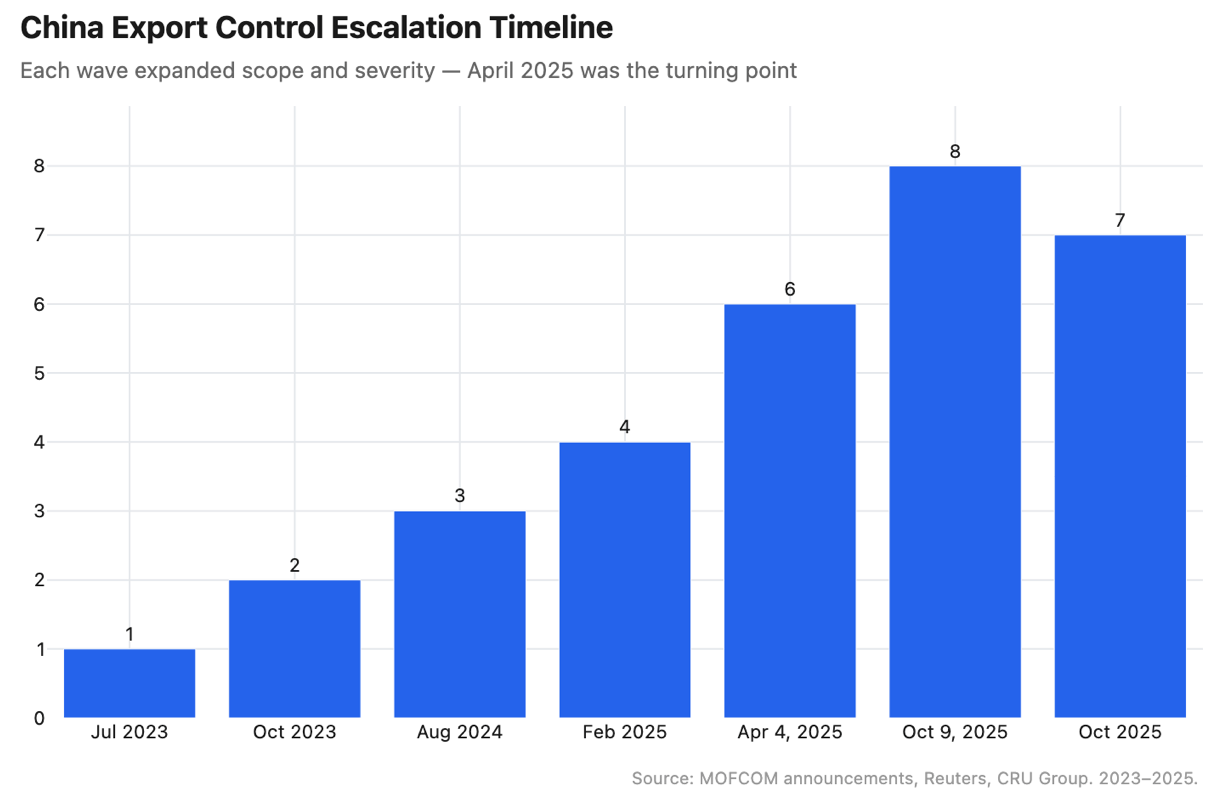

The Export Control Escalation — A Pressure Cooker Timeline

China didn’t flip the switch on April 4. They spent 18 months building the mechanism first. We need to understand this timeline because it reveals intent — and because every escalation was bigger than the last.

July 2023: gallium and germanium export controls. A test balloon. October 2023: graphite. August 2024: antimony. February 2025: tungsten, tellurium, bismuth, molybdenum, and indium. Tungsten prices tripled. Each wave was a message — we control the inputs your industry depends on, and we can cut them off whenever we want.

Then came April 4. MOFCOM Announcement No. 18. Seven heavy rare earths — samarium, gadolinium, terbium, dysprosium, lutetium, yttrium, scandium — restricted under non-automatic export licenses. Every compound, every metal, every magnet containing these elements. Case-by-case review. 60 to 120 day processing times. Military-adjacent applications? Almost never approved.

Effective immediately. No grace period. No stockpiling window. Companies with magnets already on order found their shipments frozen at customs.

But the real escalation came six months later. October 9, 2025: China introduced a Foreign Direct Product Rule for rare earths. Any magnet manufactured anywhere in the world containing even 0.1% Chinese-origin rare earth materials required Chinese government approval to export. This mirrors the US FDPR rules applied to Huawei — but applied to minerals. The nuclear option.

To put the FDP rule in perspective: there is essentially no NdFeB magnet on Earth that doesn’t contain at least trace amounts of Chinese-origin rare earths. China controls 91% of global rare earth refining and separation capacity. Even magnets manufactured in Japan, Germany, or the United States use feedstock that at some point passed through Chinese processing infrastructure. The 0.1% threshold was designed to capture everything. It mirrors the US FDPR on Huawei with surgical precision — Beijing studied Washington’s playbook and applied it to minerals.

Then, a reprieve — sort of. November 2025, Trump-Xi meeting in South Korea. China agreed to suspend export controls for one year, roughly through October 2026. Trump declared all rare earth issues settled. Markets exhaled.

But the suspension is fragile. China tightened controls on dual-use goods to Japan in January 2026. US imports of Chinese rare earth magnets fell 11% in November 2025 versus the prior year. EU imports surged 60% in the same period — Beijing using supply allocation as a geopolitical lever, rewarding allies and punishing adversaries. Yttrium exports to the United States collapsed to just 17 tons over eight months (April–December 2025), down from 333 tons in the same period a year earlier.

This is not a resolution. It’s a ceasefire. And the clock is ticking.

To put these numbers in perspective: the United States imported thousands of metric tons of rare earth magnets from China in 2024. Even with the suspension in effect, 2025 imports came in meaningfully below that baseline. The supply allocation game is already in motion — Beijing is choosing who gets magnets and who doesn’t, and Washington is on the losing end of that equation.

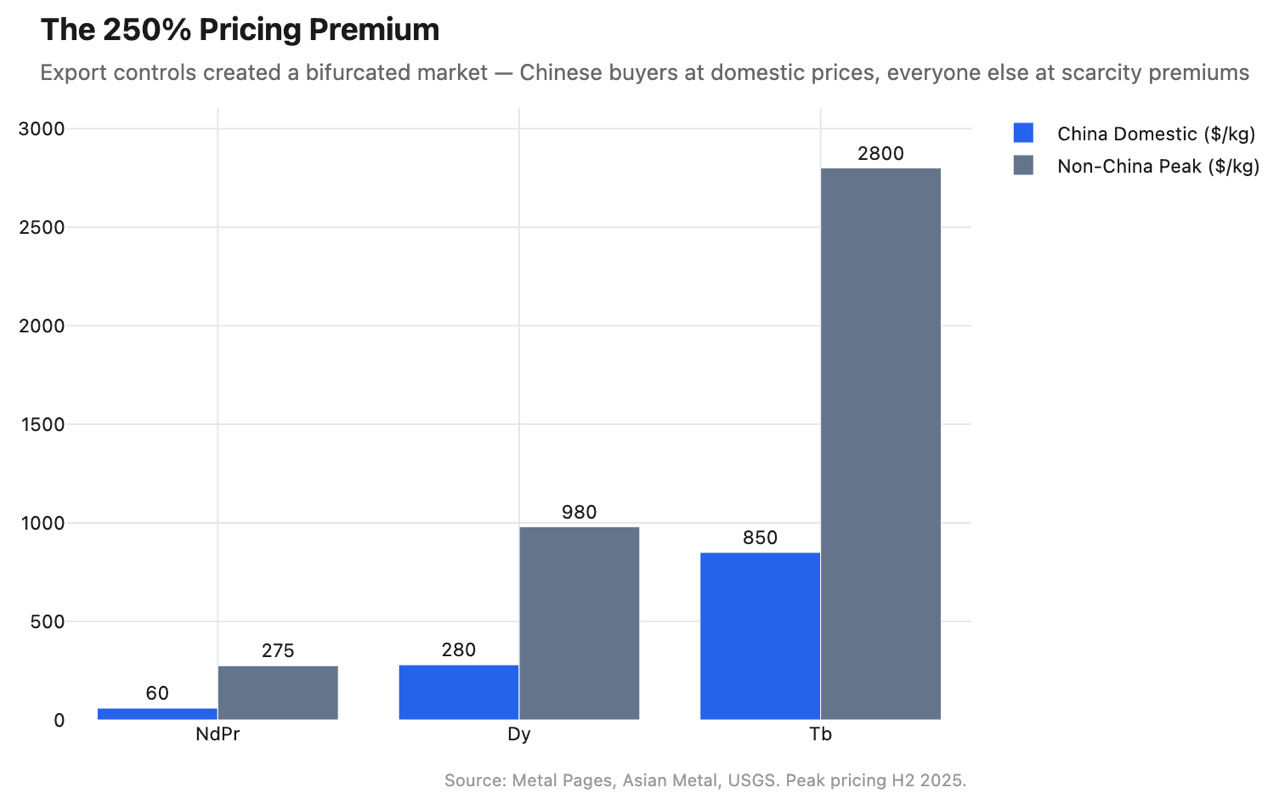

The 250% Price Premium — A Bifurcated Market

Here is the number that should keep every robotics CFO up at night: 250%. That’s the premium non-Chinese buyers paid for NdPr — the key rare earth input for NdFeB magnets — during peak restrictions in the second half of 2025.

Chinese domestic NdPr price: roughly $60 per kilogram. Non-Chinese NdPr price during the export control squeeze: $275 to $400 per kilogram. European rare earth prices hit 6x Chinese domestic levels at the peak.

This is not a tariff. Tariffs are predictable, measurable, and can be planned around. This is an asymmetric pricing structure created by export controls — Chinese manufacturers access materials at domestic prices, then export at whatever premium the licensing regime and arbitrage dictate. Chinese magnet producers operate at 20–30% gross margins. Western competitors? 10–15%, constrained by input costs that are structurally 2–4x higher.

The market is bifurcated by design. And it’s working exactly as intended.

Non-China Capacity — The Scale Problem Nobody Wants to Talk About

Every Western government has announced a rare earth independence strategy. Most of them are theater.

Total non-China NdFeB production capacity in 2025: roughly 8,000 to 12,000 metric tons per year. That’s 3 to 6% of global output. China’s current capacity: approximately 260,000 metric tons per year, expanding toward 500,000.

Here’s who’s actually building: