1X Built the Best Hand. Can They Build 10,000?

The hand race is no longer about dexterity. It's about manufacturing at scale.

1X’s NEO hand has 25 degrees of freedom, ±0.2mm accuracy, 45N fingertip force, and is IP68 waterproof. It can fold laundry, crack eggs, and assemble furniture. On paper — and in the videos — it’s the most advanced tendon-driven hand we’ve seen publicly demonstrated.

1X describes it as “an API to the physical world.” The metaphor is neat, but it misses the point.

APIs are only as good as the infrastructure behind them. And the infrastructure to manufacture this level of dexterity at scale doesn’t exist yet — not at the volumes 1X (and the rest of the industry) will eventually need.

The real question is no longer whether someone can build a highly dexterous hand. It’s whether anyone can build thousands of them at a cost that supports a viable robot business. That’s a supply chain and manufacturing problem, not an engineering one. And 1X’s own teardown quietly reveals how far the industry still is from solving it.

Read the full 1X announcement — then come back, because we’re about to unpack what they didn’t say.

What 1X Gets Right

Let’s be clear: the engineering is real. Force-controlled quasi-direct-drive tendons are not a trivial architecture. Moving from gear-driven joints to tendon-driven joints means you lose mechanical advantage and gain compliance. That trade-off only works if your control loop is fast enough, your tendons are strong enough, and your sensors are precise enough. 1X appears to have solved all three.

The shear-capable tactile sensing stack is impressive. Most dexterous hands detect normal force (pushing against a surface). Detecting shear force (sliding across a surface) is a harder problem. It requires denser sensor arrays and more complex signal processing. The fact that 1X integrated this into a hand that also hits IP68 waterproofing and food-safe compliance means they’ve solved packaging problems that most labs haven’t even attempted.

The video demonstrations speak for themselves — NEO assembling LEGO, picking up individual screws, spinning light bulbs. The visual proof is compelling.

These are not participation trophies. 1X built something that works. The question is whether they can build it at scale.

If this engineering breakdown is useful, you can subscribe for free to follow the full humanoid supply chain series.

What’s Actually Inside: Dissecting the Hand

1X TECHNOLOGIES’ CLAIM

“Every unit is built end-to-end in-house — from tendon materials and 1X Motors to the final soft polymers, skin, and tactile sensing stack.”

— 1X Technologies, NEO’s Hands

Here’s where the “end-to-end in-house” claim starts to crack. A 25-DOF tendon-driven hand has three critical component layers, each with its own supply chain dependency.

The Tendons

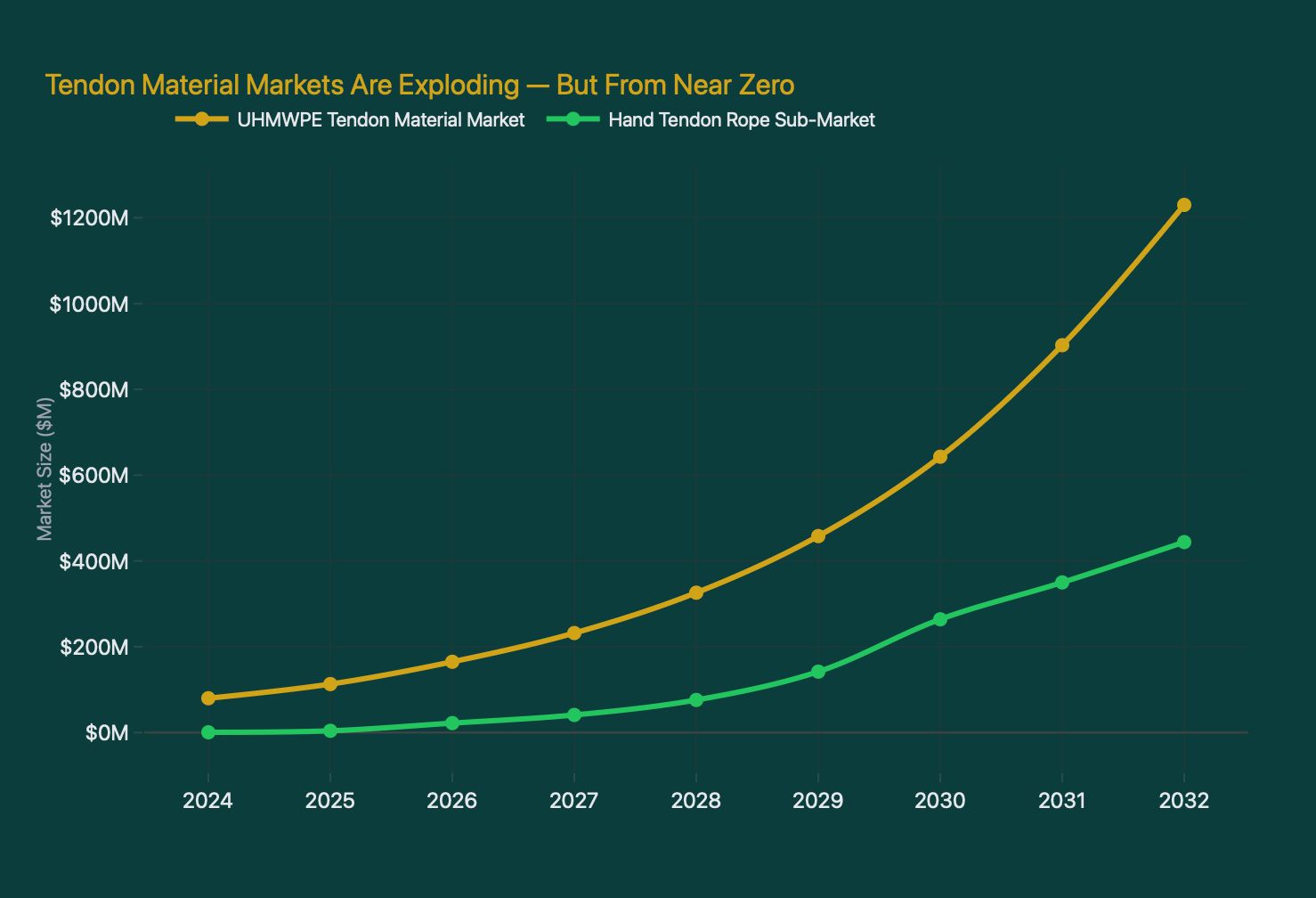

25 DOF means at least 25 tendons (most fingers need agonist-antagonist pairs, so the real number is closer to 30-40). Each tendon requires specialty ultra-high-molecular-weight polyethylene (UHMWPE) fiber. The UHMWPE tendon material market was $113 million in 2025. QY Research projects it hits $1.23 billion by 2032 at a 40.6% CAGR. That explosive growth curve proves one thing: the market doesn’t exist at scale today.

The dexterous hand tendon rope sub-market is even more extreme. IntelMarketResearch pegs it at $0.6 million in 2024, reaching $444 million by 2032 at an 86.1% CAGR. That’s a market growing from essentially zero. Carl Stahl Group leads the micro wire rope niche (0.075mm-9mm diameter). Tesla Optimus Gen3, Shadow DEX-EE, and LinkerBot L30 all depend on the same supply chain. At 10,000 hands (250,000+ tendons minimum), 1X competes with every other humanoid maker for the same material from the same suppliers.

The Motors

1X claims proprietary motors. We believe them. To a point. The motor itself may be designed in-house, but hollow-cup motors depend on precision magnets, micro windings, and encoders from a concentrated supplier base. The motor isn’t the bottleneck. The motor components are. Neodymium-iron-boron (NdFeB) magnets for micro-actuators come from a handful of suppliers. Precision wire winding for micro-motors is a specialized process with limited global capacity. 1X can design the motor. They cannot manufacture every sub-component internally. No one can.

Tesla’s approach is instructive: all 50 actuators in Optimus Gen3’s forearm, driving the hand via three ultra-thin tendons per finger. That architecture concentrates the complexity in the forearm where space is less constrained. 1X distributes motors throughout the hand itself. Both approaches work. Both depend on the same upstream component suppliers.

The Sensors

Each NEO hand needs multiple sensing modalities. Kunwei Technology (Beijing) raised ¥100 million in Series B+ funding in March 2026 specifically to scale humanoid force/torque sensor production. Each humanoid needs 2-6 wrist/ankle F/T sensors plus 28+ torque/pressure sensing elements across the body, requiring 10-30 signal chain ICs per production unit. The signal chain (analog front-end, ADC, digital processing) is where the real cost and complexity live, not the sensor element itself.

1X’s quasi-direct-drive architecture reduces the need for discrete joint torque sensors (tendon tension can be inferred from motor current). That’s a real architectural advantage. But wrist-level F/T sensing and the tactile skin stack are non-negotiable. Shear-capable tactile sensing requires dense arrays of micro-force sensors, each with its own signal processing. At 10,000 units, you need millions of these sensor elements. The supply chain for that doesn’t exist yet.

Nobody’s talking about this. The same UHMWPE tendon material that 1X needs for 250,000+ tendons is the same material every other humanoid maker needs. Carl Stahl leads this niche. The market is $113M today and needs to hit $1.23B by 2032 to meet demand. And 1X wants 10,000 hands by December.

BOM Reality Check: $20K Robot, $5K Hands

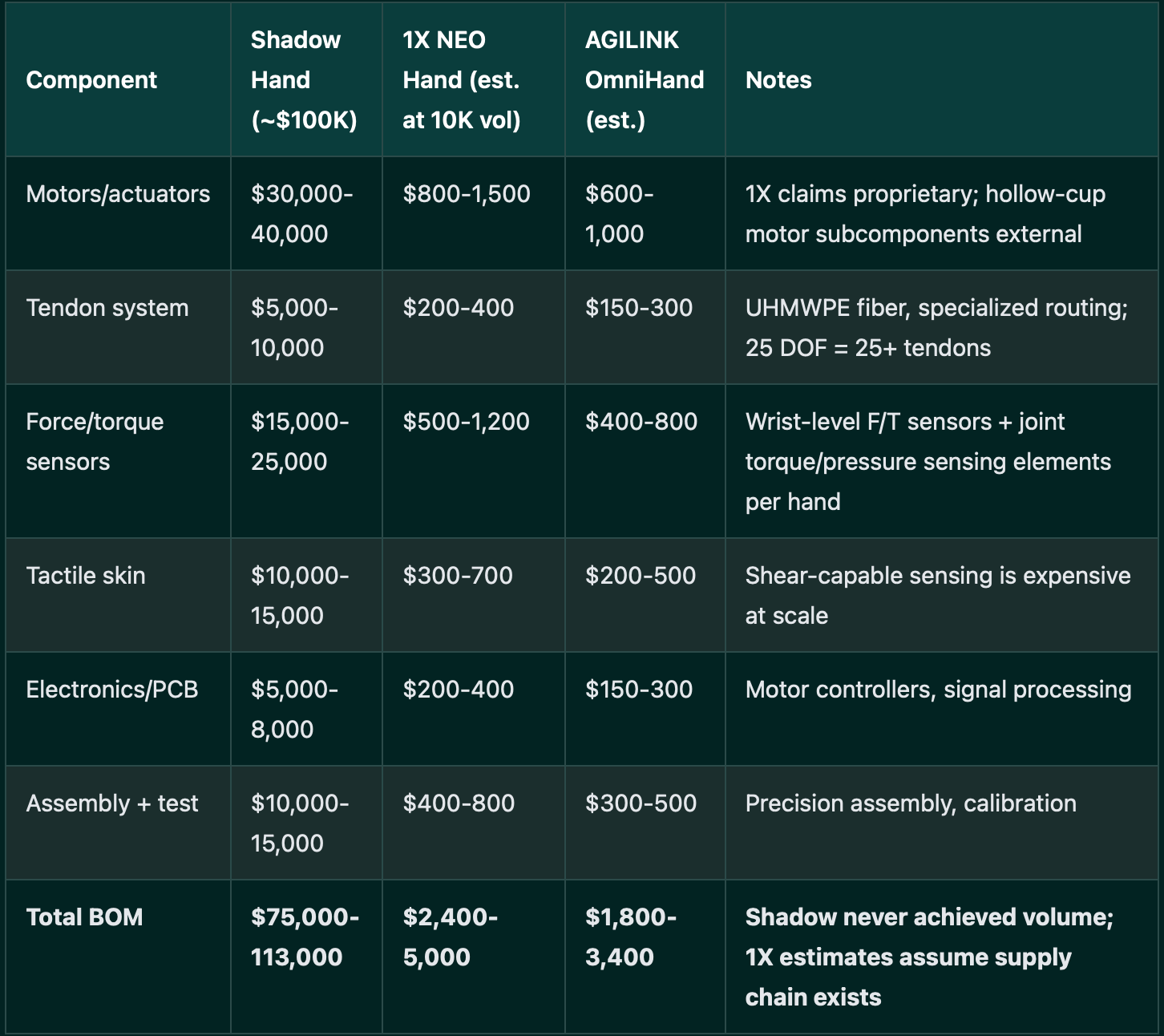

Let’s do the math. What does a 25-DOF tendon-driven hand actually cost to build at 10,000-unit volume? We built a component-level BOM estimate. The numbers are not encouraging for anyone betting on a $20,000 consumer robot.

To understand why BOM matters, meet the two hands bracketing this market. Shadow Hand has been the research benchmark for 20 years — roughly $100K per unit, never manufactured at volume, used in university labs worldwide. At the other end, AGILINK OmniHand (AGIBOT’s spin-off) has already shipped 8,000+ units with 20 active DOF, making it the closest thing 1X has to a volume rival.

The Shadow Hand costs $100,000+ because it’s built in batches of dozens. The BOM collapse from $100K to $3-5K at 10,000 units is real. But only if the supply chain scales to support it. Our estimate puts 1X’s hand BOM at $2,400-5,000 per unit at 10,000 volume. That’s 12-25% of a $20,000 robot’s total BOM, consumed by the hands alone. For a $30,000 robot, it drops to 8-17%. Neither number is catastrophic, but both assume the UHMWPE, the hollow-cup motor subcomponents, and the tactile sensor arrays are available at those volumes. They aren’t today.

AGILINK’s OmniHand comes in lower ($1,800-3,400 estimated) because 20 DOF requires fewer tendons and simpler sensor arrays. The 5-DOF difference between 20 and 25 sounds small. It isn’t. Each additional DOF adds a tendon, a motor, a sensor channel, and a control loop. The cost delta compounds.

Who’s Actually Scaling

Three players. Three very different manufacturing realities.

AGILINK (the AGIBOT spin-off) claims 8,000+ OmniHand units shipped with 20 active DOF. If that number is accurate, AGILINK has manufactured more dexterous hands than every other company on the planet combined. They achieved unicorn status (over $1B valuation) in 2026. The OmniHand is simpler than 1X’s hand, fewer DOF, no shear-capable tactile skin, lower force output. But it ships at volume. In manufacturing, shipping beats spec sheets.

Shadow Robot has been the research benchmark for two decades. The Shadow Dexterous Hand has 24 DOF and costs over $100,000 per unit. Shadow has never manufactured at volume. Not because the engineering is bad, because the economics don’t work at low volume, and the supply chain to support high-volume production wasn’t built. Shadow is a cautionary tale: the best hand in the world means nothing if you can’t make 1,000 of them.

1X targets 10,000 hands in 2026. That’s a bold claim. It requires scaling from essentially zero production to 10,000 units of the most complex dexterous hand ever designed, in roughly six months, while competing with every other humanoid maker for the same UHMWPE, the same hollow-cup motor subcomponents, and the same sensor arrays. We’ve seen this movie before. It usually ends with revised targets and a blog post about “iterating on manufacturing processes.”

What This Means for the Industry

The hand race has shifted from a dexterity competition to a manufacturing competition. The winners won’t be whoever has the best demo video. They’ll be whoever controls the tendon supply chain, the F/T sensor manufacturing base, and the hollow-cup motor component ecosystem.

Watch the component suppliers, not the hand assemblers. Carl Stahl Group leads the micro wire rope niche today. If humanoid production scales to hundreds of thousands of units per year, the tendon material supply chain becomes a chokepoint. Kunwei Technology’s ¥100M Series B+ signals that smart money is already flowing into F/T sensor manufacturing capacity. The NdFeB magnet market for micro-actuators is another constraint that nobody’s pricing into humanoid valuations.

We’ve spent months mapping the humanoid robotics supply chain — the BOM breakdowns, the component bottlenecks, the suppliers positioned to win as production scales. If you want to understand where the value actually concentrates in this market, start with our supply chain deep dive series. The hand race is just one chapter in a much bigger story about who captures margin when robots finally leave the lab.

The Hand Race Is a Manufacturing Race

1X built something extraordinary. The NEO hand is the most dexterous tendon-driven hand ever demonstrated on video. We don’t dispute the engineering. We dispute the implication that engineering excellence translates directly to manufacturing readiness.

That’s the right way to think about it. The NEO hand is a true instrument. The question is who can manufacture true instruments by the thousands, not who can build one by hand. And that question points directly at the companies building the component supply chain, not the OEMs assembling the final product.

The gap. Between “most advanced hand ever demonstrated” and “most advanced hand ever manufactured at scale” lives the entire story. AGILINK has shipped 8,000+ hands. Shadow has 20 years of R&D and zero volume. 1X wants 10,000 by December with the most complex hand ever designed. One of these timelines will prove accurate. We don’t think it’s 1X’s.

The hand race is a manufacturing race now. And manufacturing races are won by whoever owns the supply chain, not whoever owns the best design. The tendon material, the motor components, the sensor ICs: that's where the real leverage lives.

Related Reading

The Actuator Cartel — Who actually controls the motors, reducers, and drive systems every humanoid depends on

The Magnet Nobody Talks About — Why NdFeB supply is the hidden bottleneck behind every robot motor

Tesla, Figure, and Unitree’s Supplier Wars — The supplier-level competition for the same components 1X needs

The Sensor Nobody Covers Series — The tactile sensor supply chain behind the BOM table in this article

Frequently Asked Questions

If 1X’s hand BOM is $3-5K at volume, can they hit a $20K robot price?

The hand alone consumes 12-25% of the $20K target. Add legs, torso, battery, compute, and software, and the total BOM likely exceeds $15K at 10,000-unit volume. That leaves thin margin for a consumer product. 1X’s $499/month subscription model (confirmed by Forbes) makes more sense than the $20,000 purchase price. It front-loads the hardware cost into recurring revenue.

Is AGILINK a serious competitor to 1X in dexterous hands?

AGILINK has shipped more dexterous hands than anyone. Their OmniHand is simpler (20 DOF vs 25 DOF), lower force, no shear-capable tactile skin. But manufacturing volume is manufacturing volume. In a market where supply chain control determines winners, the company that’s already shipping 8,000+ units has a structural advantage over the company targeting 10,000 by December.

Why does the tendon supply chain matter so much?

UHMWPE tendon material market is $113M today. It needs to hit $1.23B by 2032 to meet projected humanoid demand. That 10x growth in seven years requires massive capacity expansion. If capacity lags demand, tendon prices spike, margins compress, and production targets slip. Every humanoid maker depends on the same material. The tendon market is the bottleneck nobody’s pricing into humanoid stocks.

Should investors focus on humanoid OEMs or component suppliers?

Component suppliers. The tendon material, F/T sensor, and micro-motor subcomponent companies capture margin regardless of which humanoid OEM wins. Carl Stahl Group, Kunwei Technology, and NdFeB magnet manufacturers are picks-and-shovels plays on humanoid scaling. Hand assemblers compete on price. Component suppliers compete on capacity. And capacity is scarce.

What’s the most overhyped claim in 1X’s NEO hands announcement?

“End-to-end in-house.” 1X designs the hand. They don’t mine the UHMWPE, manufacture the hollow-cup motor subcomponents, or fabricate the tactile sensor arrays. “End-to-end” means they assemble the hand in-house using components from external suppliers. That’s integration, not vertical integration. The distinction matters when the supply chain is the constraint.

Where does Tesla Optimus fit into the hand race?

Tesla’s Gen 3 hand promises 22 degrees of freedom with a tendon-driven architecture — three thin tendons per finger, all 50 actuators relocated to the forearm. On paper, it’s the most direct competitor to 1X’s approach. In practice, Tesla has delayed the Gen 3 unveiling repeatedly and has not demonstrated the hand publicly. The patent filings are detailed. The working hardware is not. Tesla’s vertical integration gives them a structural advantage if they can execute — they design their own actuators, control systems, and manufacturing processes. But until we see a Gen 3 hand picking up screws on video, Tesla remains the elephant in the room: the competitor everyone assumes will arrive, but nobody can point to.