Actuators Part 1: The Cartel

The hidden chokepoint behind every humanoid robot — and the four companies that control it.

The Actuator Cartel — A 5-Part Series

1. Who Controls the Robot Muscle Supply Chain

2. From Harmonic Drives to Torque Motors

3. The Chinese Are Coming

4. Tesla, Figure, and Unitree’s Supplier Wars

5. The Actuator Cartel’s Endgame

I was standing in a factory in Suzhou last autumn, watching a machine the size of a small car slowly wind a coil of precision-ground steel wire around a flexspline. The operator, a woman in her fifties with reading glasses perched on her nose and the calm, deliberate movements of someone who has done this exact thing ten thousand times, adjusted a dial with the kind of precision you’d expect from a brain surgeon. She caught me staring and smiled. “This part,” she said, tapping a component no bigger than a coffee mug, “goes into the knee of a Tesla robot.” She said it the way someone might mention their daughter got into a good university, quiet pride, no fanfare, back to work.

That coffee-mug-sized piece of metal is called a harmonic reducer, and if you’ve been following the humanoid robot story at all, you know it’s one of the most bottlenecked components in the entire supply chain. A humanoid robot needs somewhere between 14 and 40 rotary actuators, depending on how many joints the designers want to articulate, wrists, elbows, shoulders, knees, ankles, fingers. Each one of those joints needs something that can deliver high torque in a tiny package, with almost zero backlash, for hundreds of thousands of cycles. Each one costs anywhere from $200 to $800 at the volumes we’re talking about today. Do the math on a million robots and you’re looking at a multi-billion-dollar addressable market just for these little metal canisters full of precision gears.

But that I find wild: there are maybe four companies on Earth that can make these things at the quality and scale the humanoid robot industry needs. Two of them are in the same Japanese prefecture, an hour’s train ride from each other, with a combined century of institutional knowledge that you can’t reverse-engineer from a teardown video on YouTube. And the market, hasn’t fully priced what that concentration means.

who these people are, what they’re building, and why the single most important bottleneck in the humanoid robot buildout might be hiding in a factory in Nagano Prefecture.

How We Got Here

In 1955, a young American engineer named C. Walton Musser filed a patent for something he called “strain wave gearing.” Musser was working for United Shoe Machinery Corporation at the time, a name that tells you exactly what kind of world this was invented in, and he had been thinking about a problem that seemed almost absurdly niche: how do you transmit motion through a flexible metal cup in a way that eliminates backlash entirely?

The idea was elegant in that mid-century engineering way. Instead of meshing rigid gear teeth directly against each other, the way gears had worked since the Greeks. Musser imagined a flexible cup, a flexspline, with teeth on its outer rim. Inside this flexspline sits an oval-shaped wave generator. As the wave generator rotates, it deforms the flexspline, creating a wave pattern where the flexspline’s teeth engage with a rigid outer ring at two opposite points. Because the flexspline has slightly fewer teeth than the outer ring, every rotation of the wave generator advances the flexspline by a tiny amount relative to the ring.

What you get is a gearbox with almost zero backlash, remarkable precision, and a torque-to-weight ratio that conventional gears can’t touch. It is, in its quiet way, one of the cleverest mechanical inventions of the twentieth century.

Musser licensed the patent to a small Japanese company that had been founded in 1970 in the city of Hotaka, Nagano Prefecture, a place better known for its mountains and apple orchards than for precision engineering. That company was Harmonic Drive Systems. They spent the next fifty years turning Musser’s elegant idea into something you could actually manufacture at scale, with tolerances measured in microns and failure rates measured in single-digit percentages after tens of thousands of hours of operation.

What happened next is a story that should be familiar to anyone who has studied Japanese manufacturing. The precision machinery industry that emerged in Japan after the war, companies like NSK, THK, Fanuc, and yes, Harmonic Drive Systems, didn’t just copy Western technology. They refined it obsessively. The metallurgy got better. The heat treatment got more precise. The surface finishing became almost artisanal. Over decades, they built a body of tacit knowledge, the kind you can’t write down in a textbook, the kind that lives in the fingertips of the woman at the winding machine, that created a moat far deeper than any patent.

This is the thing about the actuator supply chain that I think gets missed in most analyst reports. You can buy a harmonic reducer on AliExpress for $80 and it will look exactly like the one from Harmonic Drive Systems. It might even work for a while. But the difference between “works for a while” and “works for 15,000 hours without losing precision” is everything, and it lives in details that don’t show up in photographs.

The Setting: A Market That Doesn’t Exist Yet

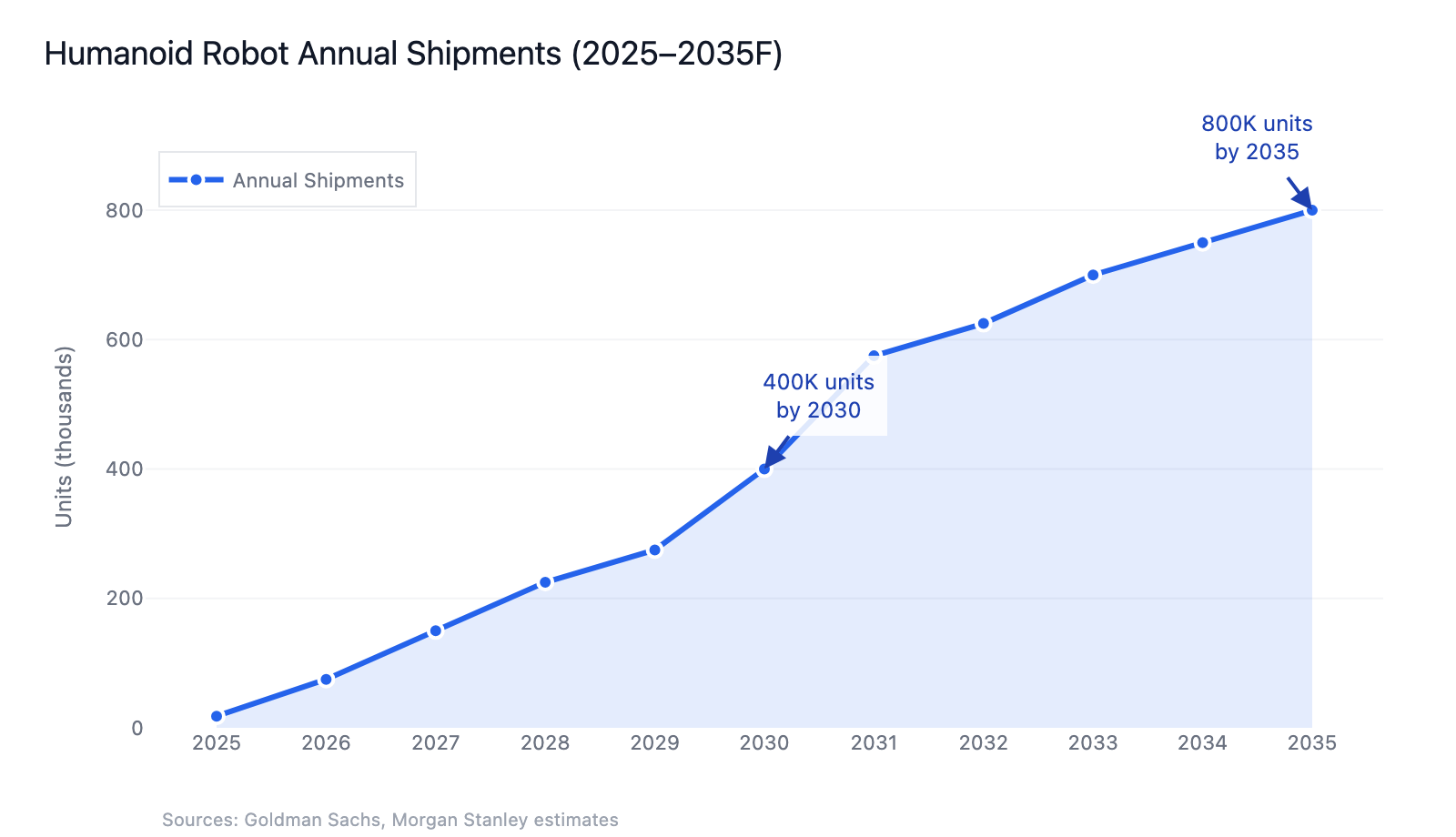

Goldman Sachs thinks we’ll ship somewhere between 50,000 and 100,000 humanoid robots in 2026. By 2030, they see 250,000 to 400,000 units annually. Morgan Stanley, never ones to be outdone on the art of the bold prediction, published a note suggesting upwards of 800,000 units by 2035 and a total installed base of over a billion robots by 2050, a market they frame at roughly $5 trillion.

Now, a billion robots by 2050. I don’t know if that number is right, nobody does, but let me try to put the ramp in perspective. In 2025, the entire industry produced maybe 18,000 humanoid robots. Most of those went to internal R&D programs, university labs, or carefully managed pilot deployments. We’re talking about going from 18,000 units, essentially a research curiosity, to something approaching a mass-manufactured product category in about five years.

That’s faster than the iPhone ramp from 2007 to 2012. Faster than electric vehicle adoption from 2015 to 2020. Faster than basically any hardware category I can think of, with the possible exception of drones, and drones don’t need precision harmonic drives in every joint.

And every single one of those robots needs actuators. Not just any actuators, precision rotary actuators capable of delivering high torque in a package small enough to fit inside a human-sized knee joint, with feedback sensors accurate enough to let the robot know how hard it’s gripping an egg without turning it into breakfast, and reliable enough to function for thousands of hours in factory environments full of dust, vibration, and thermal cycling.

Let me pause and explain what an actuator actually is, because I think most of us picture a motor and call it a day. An actuator is really three things bundled together. First, the motor, that’s the raw power source, converting electricity into rotation. Second, the gearbox, usually a harmonic drive or a planetary gear system, that translates high-speed rotation into the slow, forceful, precisely controlled motion a robot joint needs. Third, the sensors, encoders and torque sensors that tell the robot’s control system where the joint is in space and how much force it’s exerting.

Think of it as the muscle, the tendon, and the nerve ending of a robot joint, all in one package. The motor provides the power. The gearbox provides the mechanical advantage. The sensors provide the feedback. Miss on any one of these three and the robot either can’t move, can’t move precisely, or doesn’t know where it is.

It’s the gearbox part that’s the real chokepoint. And that’s where our story gets interesting.

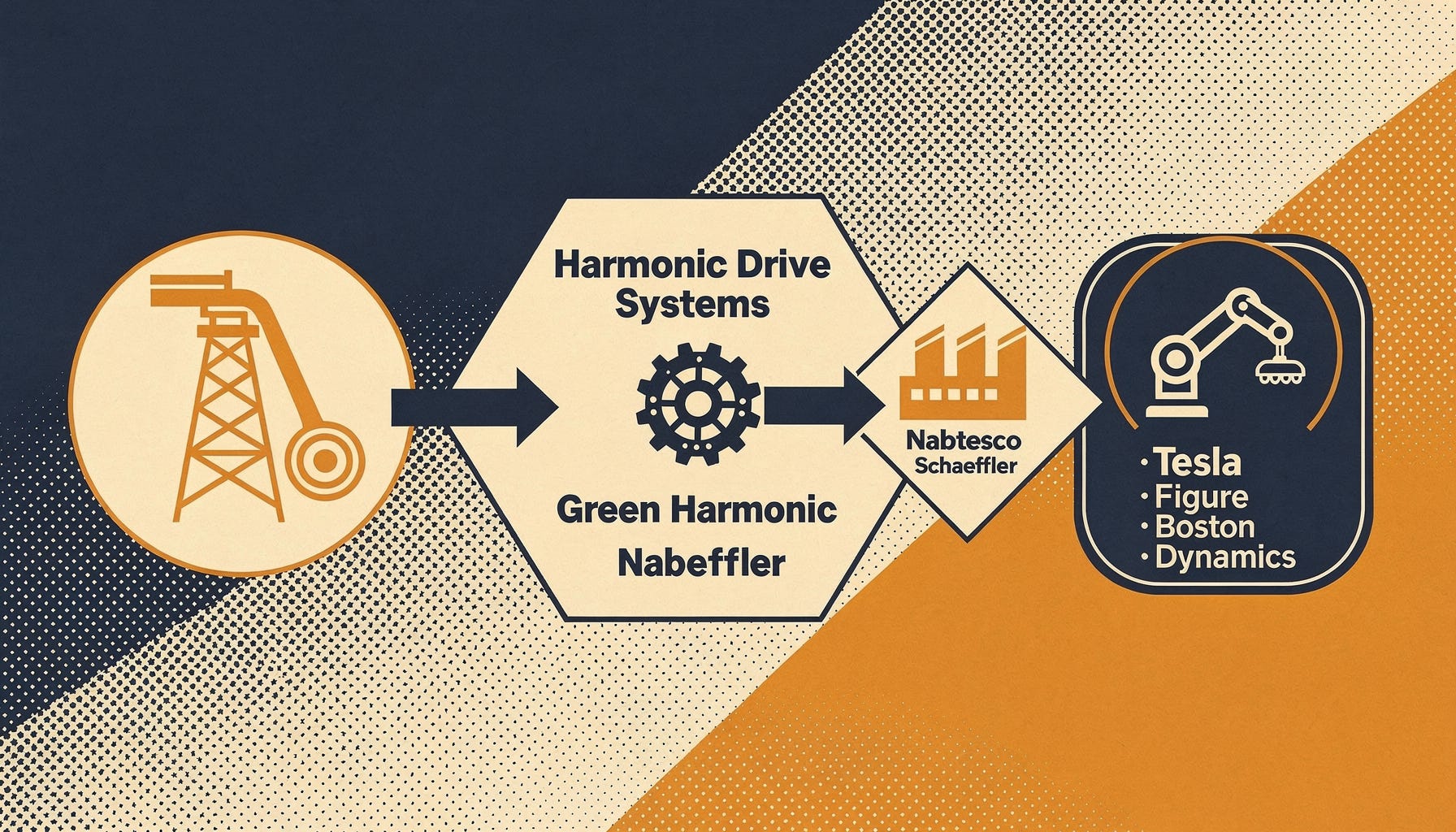

The Characters: Four Companies, Four Stories

Harmonic Drive Systems. The Original (6324.T)

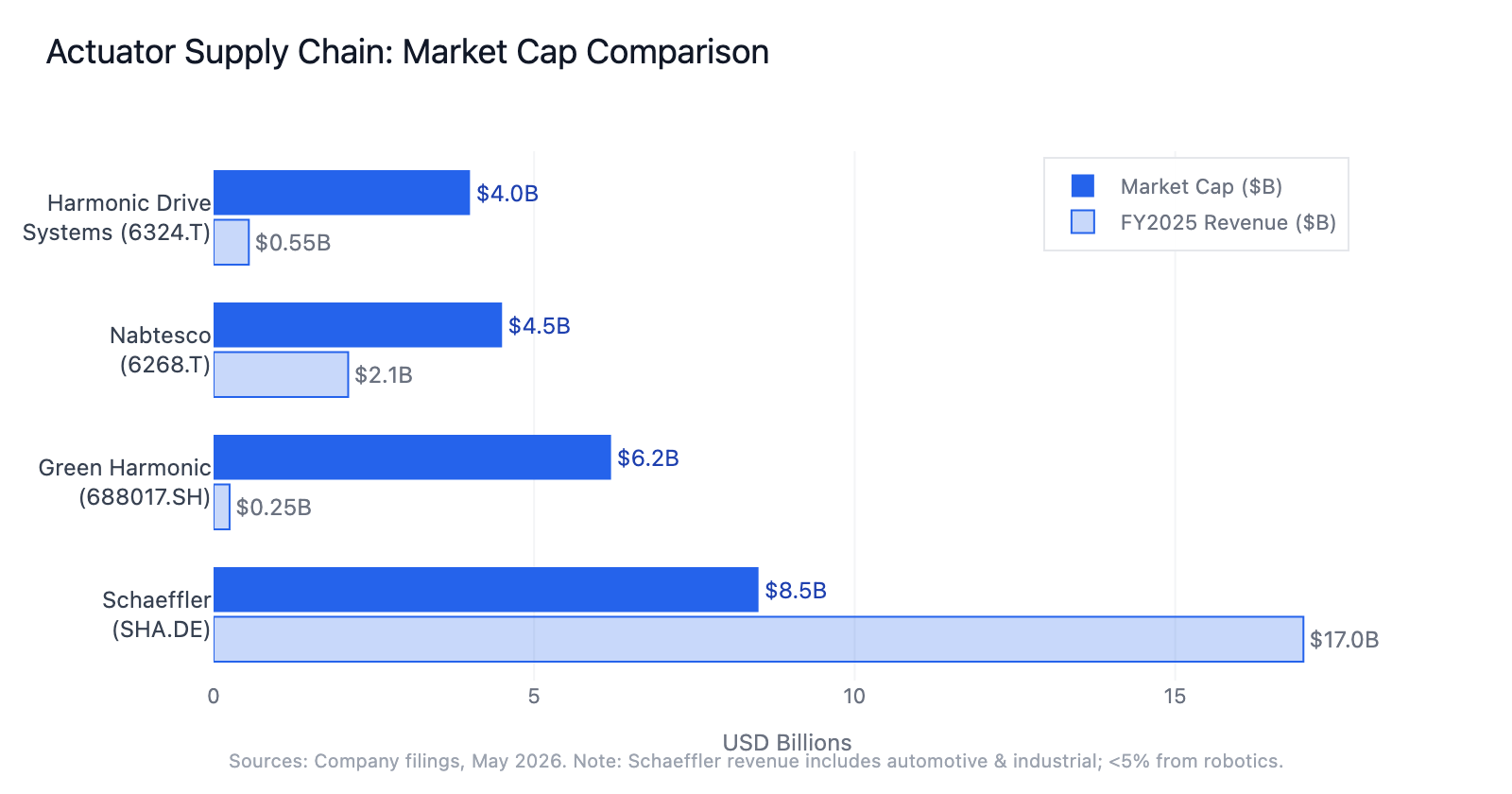

Harmonic Drive Systems is not a big company, at least not by the standards of the global industrial economy. It’s headquartered in Hotaka, a small city in Nagano Prefecture surrounded by the Japanese Alps, and it employs maybe 4,000 people. Its market cap hovers around ¥590 billion, or roughly $4 billion. It does not make headlines. It does not give splashy presentations at CES. It makes harmonic reducers, obsessively, for over fifty years.

I’ve never been to their factory in Hotaka, but I imagine it feels like visiting a Swiss watchmaker. The floors are probably immaculate. The air is probably climate-controlled to within half a degree. Every machine operator probably has a decade of experience and a quiet, almost spiritual relationship with their dial indicators and micrometers. This is not a place that panics. This is a place that has seen industrial booms come and go, the automotive automation wave, the electronics assembly boom, the collaborative robot wave, and has expanded capacity each time in the careful, deliberate way of a company that knows its value and isn’t in a hurry to prove anything to anyone.

Harmonic Drive Systems’ FY2025 results showed the kind of steady, boring excellence you want from a precision manufacturer: revenue growing in the high single digits, margins holding firm, and a backlog that, according to people I’ve spoken with, is starting to include real volume from humanoid robot programs. Their stock is up about 9% in the past twelve months, a nice return, but nothing like the triple-digit moves some of the AI plays have delivered.

But about Harmonic Drive Systems that I find fascinating. They are expensive, and they know they’re expensive. When Tesla’s procurement team first came knocking for Optimus components, the price tag reportedly gave them pause. These are the Cadillac option, the thing you buy when failure is not an option and you need the part to work for 15,000 hours without degradation. And in a funny way, their expensiveness is their moat. They have spent fifty years building the institutional knowledge that lets them charge those prices, and nobody, not even the very motivated engineers in Suzhou, can replicate that overnight.

Green Harmonic. The Disruptor (688017.SH)

About 1,500 kilometers west of Hotaka, in the industrial sprawl of Suzhou, a very different kind of company has been doing something remarkable. Leader Harmonious Drive Systems, or Green Harmonic, as they’re known in English, was founded in 2011 by a pair of brothers who saw an opportunity in China’s growing industrial robot market. They started out making harmonic reducers for Chinese industrial robot manufacturers who couldn’t afford Japanese prices. Their first products were, by all accounts, not great. But they kept at it.

Fourteen years later, Green Harmonic is Tesla’s primary harmonic reducer supplier. When Musk’s team placed that massive $685 million order with Sanhua Intelligent Controls for Optimus linear actuators, the rotary joints, the ones that actually need harmonic drives, were coming from Green Harmonic. The company delivered batches sufficient for approximately 700 Optimus robots in Q2 2025 alone. Their new Suzhou factory, scheduled to open later in 2026, will have capacity for 500,000 units per year.

Let that number sit for a second. Five hundred thousand harmonic reducers per year. That’s enough for roughly 35,000 humanoid robots, assuming fourteen reducers per robot. It’s a staggering ramp for a company that was essentially unknown outside of Chinese industrial circles five years ago.

Green Harmonic’s stock, listed on Shanghai’s STAR Market as 688017, has been on a tear, up about 40% in the past year. The brothers who founded it are now billionaires, which is the kind of wealth creation story that makes you think maybe you should have paid more attention to Chinese industrial automation stocks in 2020. Their market cap, at roughly ¥45 billion or $6.2 billion, actually exceeds Harmonic Drive Systems’, a remarkable inversion for a company that, by its own admission, is still closing the quality gap with the Japanese incumbent.

The question, of course, is whether they can maintain quality at that scale. Japanese manufacturers have spent decades refining the metallurgy, the heat treatment processes, the surface finishing, all the invisible details that determine whether a harmonic reducer lasts 10,000 hours or fails catastrophically at hour 500. Green Harmonic’s bet is that they can close that gap faster than the market can demand perfection. So far, Tesla seems willing to take that bet. But if quality issues emerge at scale, and in precision manufacturing, they almost always do, the narrative shifts quickly.

Nabtesco. The Quiet Giant (6268.T)

If Harmonic Drive Systems is the specialist and Green Harmonic is the disruptor, Nabtesco is the industrial conglomerate that happens to be very, very good at precision motion control. Formed in 2003 from the merger of Teijin Seiki and NABCO, Nabtesco is best known for its RV reducers, a different type of precision gearbox used in the larger joints of industrial robots, particularly the shoulders and hips, where you need more torque than a harmonic drive can comfortably provide.

Nabtesco reported FY2025 revenue of ¥307.9 billion, or about $2.1 billion, with net income of ¥15.7 billion. Their operating profit jumped 65% in the first half of 2025, one of those numbers that makes you sit up in your chair a little. The company trades at roughly ¥5,600 per share, with a market cap of about ¥656 billion, or $4.5 billion.

What’s fascinating about Nabtesco, and this is one of those details that I think tells you a lot about how Japanese industrial companies think, is their relationship with Harmonic Drive Systems. The two companies formed a strategic alliance in 2005, a kind of gentleman’s agreement to not step on each other’s toes too much. Harmonic Drive would focus on the smaller, higher-precision harmonic reducers. Nabtesco would focus on the larger, higher-torque RV reducers. Together, they effectively controlled the global precision reducer market for industrial robots.

That alliance was dissolved in 2022. And by January 2025, Nabtesco had fully divested its approximately 19% stake in Harmonic Drive Systems, a sale that netted roughly $357 million. These two companies, which spent nearly two decades as partners and cross-shareholders, are now independent competitors in a market that’s about to get dramatically bigger. I find that timing interesting.

Nabtesco’s management, in that restrained Japanese way, has been hinting at capacity expansion for humanoid robot demand. They’re not making the kind of splashy announcements that Green Harmonic is, that’s not how Japanese industrial companies operate, but they’re also not a company that panics. They’ve seen robot cycles before. Each time, the cycle comes, they expand capacity, capture market share, and emerge stronger. I suspect they’re doing it again.

Schaeffler. The German Entrant (SHA.DE)

At CES 2026 in Las Vegas this January, a German automotive and industrial supplier called Schaeffler did something that made the entire robotics industry sit up and take notice. They unveiled a planetary gear actuator, not a concept, not a rendering, but a production-ready unit, specifically designed for humanoid robots. It combined a two-stage planetary gearbox, an electric motor, an encoder, and a controller in a package small enough to fit inside a robot’s thigh.

Schaeffler is not a small company. They’re a €20+ billion industrial conglomerate with deep expertise in bearings, transmission systems, and precision manufacturing. They make the kind of components that have to work perfectly for the lifetime of a car engine or a wind turbine, a hundred thousand hours of continuous operation in hostile environments. That expertise, it turns out, transfers remarkably well to the problem of building robot muscles.

Here’s the claim that Schaeffler has been making, and I think it’s worth paying attention to: they estimate that their current and upcoming hardware portfolio, actuators, bearings, sensors, represents roughly 50% of the total material cost required to build a humanoid robot. Fifty percent. They’re targeting a multi-million-euro order book for humanoid robot components by 2030, and they’ve already announced partnerships with Humanoid, a robotics startup, and Hexagon Robotics.

The German approach is different from the Japanese in ways that matter. Where Harmonic Drive Systems and Nabtesco spent decades perfecting individual components, the flexspline, the circular spline, the wave generator bearing. Schaeffler is offering an integrated system. Motor, gearbox, sensors, electronics, all in one black-box package. It’s the kind of vertical integration that appeals to robot companies who don’t want to become actuator experts themselves and would rather just specify a part number and a torque curve and get on with building the software stack.

Schaeffler’s automotive business has been under structural pressure, electric vehicles have dramatically fewer moving parts than internal combustion engines, which is not great news if your business model is selling moving parts, and they’ve been actively looking for growth vectors. Humanoid robotics is a remarkably good fit for their capabilities. The question, as always, is whether they can execute in a new market against competitors who have been doing this for fifty years.

The Conflict: Who Gets the Muscle?

So here’s where the story gets tense, and I think this is the part that most market commentary misses. We have demand that could grow from roughly 50,000 humanoid robots in 2026 to something between 400,000 and 800,000 by 2035. And we have a supply base for precision actuators that, even with aggressive capacity expansion by all four major players, might struggle to keep up.

This is not a problem that solves itself with a bigger factory and more CNC machines. Precision gear manufacturing is constrained by something much harder to scale: people who know how to do it. The heat treatment specialist who can look at the color of a flexspline coming out of the furnace and know whether the grain structure is right. The metrology technician who can interpret a CMM report and tell you which machine tool on the line is drifting out of tolerance. The design engineer who has spent twenty years learning what happens when you change the tooth profile by half a micron.

There are maybe a few thousand people on Earth with that level of expertise, working at maybe a dozen companies, in maybe three countries. You can build a new factory in eighteen months. You can’t build a new precision gear expert in eighteen months.

Let’s look at how the major robot companies are positioning themselves around this constraint.

Tesla is the elephant in the room. Musk has said he wants to eventually build 10 million Optimus units per year. Even if he’s off by an order of magnitude, and with Musk, that’s always the question, we’re still talking about a million-unit program that would consume more harmonic reducers than the entire industrial robot industry uses today. Tesla’s approach has been a hybrid: they design their own custom actuators, integrating the motor, gearbox, and sensing into packages optimized for Optimus’s specific joint requirements, but they still rely on suppliers for the precision components inside those packages. Harmonic reducers from Green Harmonic. Linear actuators from Sanhua Intelligent Controls, under that $685 million order with deliveries starting from Sanhua’s Mexican factory in 2026. Encoders and precision bearings from undisclosed foreign suppliers, though industry sources I’ve spoken with suggest Japanese and German vendors.

Tesla’s V3 Optimus, originally expected earlier this year, has been pushed to late summer 2026, one of those quiet delays that, in the world of hardware, usually means something interesting is happening in the supply chain.

Figure AI has taken a different path. When they introduced Figure 03, they made a deliberate point of emphasizing vertical integration: actuators, batteries, sensors, structures, and electronics, all designed completely in-house. Figure raised $1 billion in their Series C round in September 2025 at a $39 billion valuation, with Intel, NVIDIA, Qualcomm, and Brookfield Asset Management all participating. At that valuation, you can afford to build your own actuator team. You can hire the precision gear experts away from the incumbents. You can build your own test lab and your own qualification infrastructure.

But about vertical integration in precision manufacturing: it’s expensive, it’s slow, and it only makes sense if you’re planning to ship at very high volumes. The Tesla Model 3 approach, own the design, own the integration, but let specialists handle the hardest manufacturing steps, is a proven template. The Figure approach, own everything, is a bet that the learning curve advantages of vertical integration outweigh the time and cost of building internal capabilities from scratch. both approaches can work, but they require very different kinds of companies to execute.

Boston Dynamics has perhaps the most interesting supply chain story of the three. In January 2026, they announced that Hyundai Mobis, the parts and components division of Hyundai Motor Group, which acquired Boston Dynamics in 2021, would supply the actuators for the new Atlas robot. It’s a fascinating arrangement: the company that owns Boston Dynamics is also building the factory that makes the robot’s muscles.

Hyundai Mobis is constructing a new robotics factory capable of producing 30,000 Atlas robots per year. The 2026 production run is already fully committed to internal Hyundai pilots and a partnership with Google DeepMind. What this does, essentially, is give Boston Dynamics automotive-grade actuator manufacturing, the same quality systems, the same supply chain discipline, the same cost-down capabilities that Hyundai applies to manufacturing millions of cars, while giving Hyundai Mobis a showcase for their robotics components business. It’s the kind of industrial logic that makes a lot of sense on paper. We’ll see if it works in practice.

One detail worth noting: the Korea JoongAng Daily reported in February 2026 that prototypes of Hyundai’s Atlas and LG’s Cloid both used foreign-made actuators, specifically from Harmonic Drive Systems and Nabtesco. Even with Hyundai Mobis’s involvement, even with Korean industrial policy pushing for domestic supply chains, the Korean humanoid programs are still dependent on Japanese precision components for the hardest parts. That tells you something about the depth of the moat.

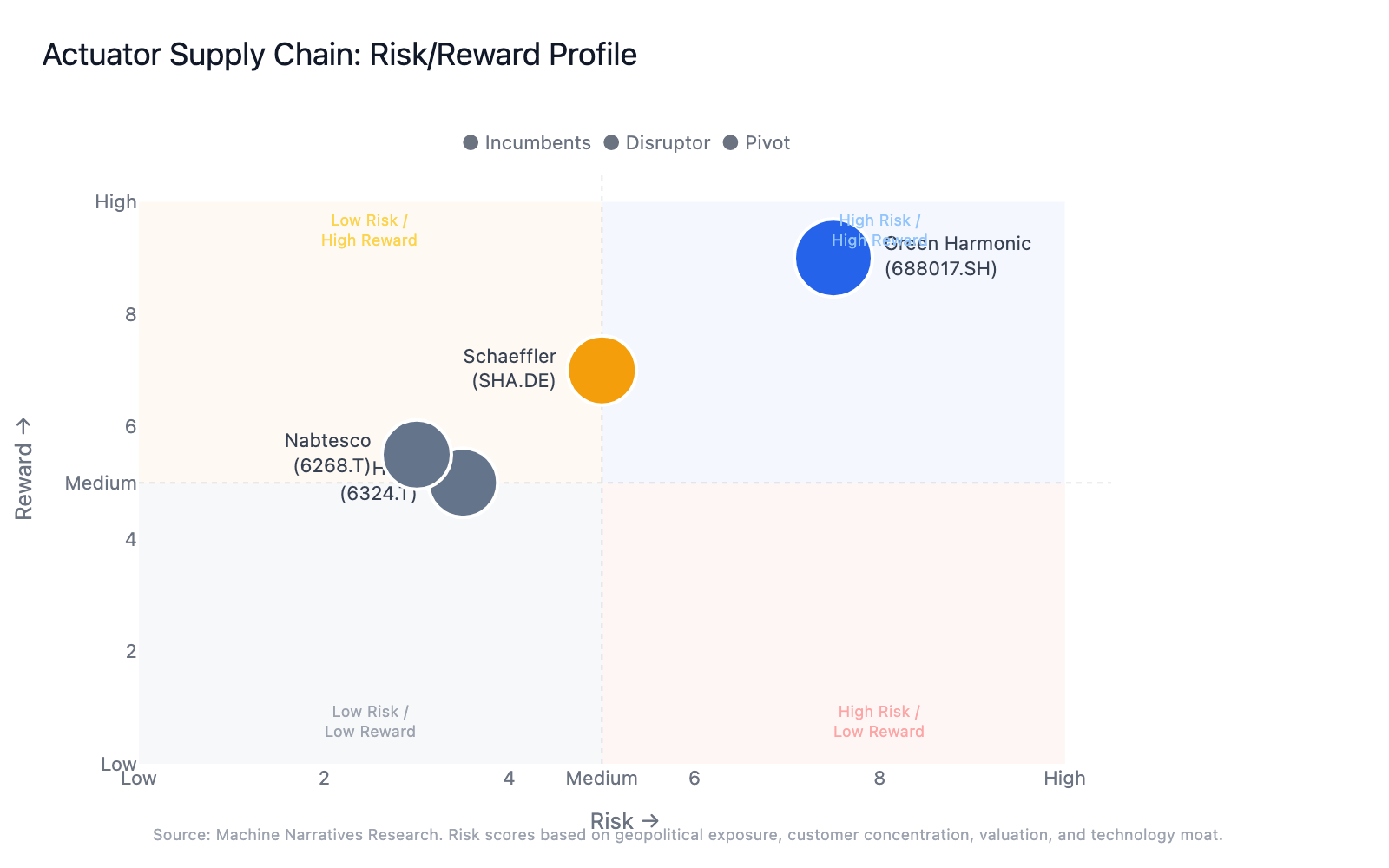

The Numbers: What This Means for Investors

Let me try to put some investable numbers around this. I'm going to focus on the publicly traded companies, because those are the ones most of us can actually buy, though I should note, as always, that I'm not giving investment advice and you should do your own work.

Table 1: Actuator supply chain — key publicly traded companies. *Chinese A-share market caps can carry local valuation premiums; compare with caution. Data approximate as of May 2026. Sources: Company filings, FactSet.

The thing that jumps out at me is how concentrated this is. You have two Japanese companies with decades of precision manufacturing expertise, one Chinese upstart with a Tesla contract and breakneck expansion plans, and one German industrial giant pivoting from automotive to robotics. That’s basically it for the precision actuator supply chain at scale. A few smaller players. Nabtesco’s Japanese competitors in the RV reducer space, some Korean and Taiwanese gear manufacturers, are trying to move up the value chain, but they’re years behind in the qualification cycles that matter for humanoid robot programs.

the investment thesis breaks down into three buckets, and each one demands a different kind of thinking.

The incumbents: Harmonic Drive Systems and Nabtesco. These are the safe-ish bets. They have the technology, the institutional knowledge, the manufacturing expertise, and the customer relationships that have been built over decades. But they’re also expensive, and they’re facing real pricing pressure from Green Harmonic and the broader Chinese industrial automation ecosystem. Their stocks have already run up on robot enthusiasm. Harmonic Drive is up about 9% over the past year, Nabtesco a bit more, and you’re paying a premium for quality and reliability. The question is whether the premium is justified by the moat, and I think it probably is, but that’s a judgment call.

The disruptors: Green Harmonic and, to a lesser extent, Sanhua Intelligent Controls. These are the growth stories. They’ve got Tesla contracts, aggressive expansion plans, and the tailwind of Chinese industrial policy that is actively trying to build domestic alternatives to Japanese precision components. But they’re also priced for perfection. Green Harmonic’s market cap already exceeds Harmonic Drive Systems’, despite meaningfully lower revenue and a quality track record that’s still being written. The geopolitical risk, tariffs, export controls, the ever-present shadow of cross-strait tensions, is real and hard to hedge. Any quality issues or delays in the Tesla Optimus ramp could hurt badly.

The pivots: Schaeffler and the broader universe of industrial companies using robotics as a growth vector. Schaeffler is interesting in a different way than the others. They’re offering integrated actuator systems rather than individual components, which could command higher margins and stronger customer lock-in over time. Their automotive heritage gives them genuine expertise in scaling precision manufacturing. But robotics is still a tiny fraction of their overall revenue, their automotive and industrial businesses dominate the P&L, so you’re buying a lot of legacy exposure to get a relatively small amount of robot upside. The thesis works, but you need patience.

What I’m Watching

I don’t have a clean answer to the question of who wins here. I don’t think anyone does. The humanoid robot buildout is the kind of industrial transformation that makes fools of forecasters, the shape of demand, the pace of adoption, the technological dead ends that nobody sees coming, all of these will surprise us.

But here’s what I do know. The actuator supply chain is the most concentrated, most bottlenecked, most strategically important piece of the humanoid robot puzzle. You can have the best AI models, the most elegant mechanical design, the slickest software stack, but if you can’t source enough precision actuators at scale, at quality, at cost, you can’t build a robot that works. And right now, four companies. HDSI, Nabtesco, Green Harmonic, and Schaeffler, control a disproportionate share of the global capacity for making these things.

They know it. The robot companies know it. I’m not sure the market has fully priced it yet.

Goldman Sachs noted in a November 2025 report that Chinese component suppliers are in what they called a “preemptive” phase, building massive production capacity ahead of a 2026 demand boom despite a current lack of large-scale orders. It’s a classic capacity race: the winners will be the ones who can actually deliver quality at volume when the orders materialize. And in precision manufacturing, the gap between “can build a factory” and “can ship parts that meet spec at 99.9% yield” is measured in years, not quarters.

I keep thinking about that woman in the Suzhou factory, the one winding steel wire around a flexspline with the concentration of a calligrapher. She probably doesn’t know who Elon Musk is, or what a “humanoid robot” looks like, or what Goldman Sachs thinks the TAM will be in 2035. But she’s making the thing that makes the thing possible. And there are maybe a few thousand people on Earth with her level of skill, working at a handful of companies, in a handful of places. Hotaka, Suzhou, Herzogenaurach, that most investors have never heard of.

That’s the actuator cartel. It’s not a formal conspiracy, nobody’s meeting in a smoky room to fix prices. It’s a concentration of expertise, built over decades, in places that don’t make headlines, manufacturing components that most people have never seen. And as the humanoid robot industry tries to grow from 50,000 units to something on the order of a million, those few companies and those few thousand workers are going to be the ones who decide whether the dream of affordable, capable humanoid robots becomes real or remains just out of reach.

I’ll be watching. And in the next piece in this series, I want to look at the harmonic drive itself, how a 1955 patent became the foundation of precision motion control, and how four decades of Japanese engineering created a moat that Chinese competitors are only now beginning to cross.

The Actuator Cartel — A Machine Narratives Series

Part 1 : The Actuator Cartel: Who Controls the Robot Muscle Supply Chain — the invisible chokepoint behind every humanoid robot by Amanda J

Part 2: From Harmonic Drives to Torque Motors — a 40-year history of precision motion control

Part 3: The Chinese Are Coming — Green Harmonic Just Hit 18% and Japan’s Dominance Has a Deadline

Part 4: Tesla, Figure, and Unitree’s Supplier Wars — case studies in actuator procurement strategy

Part 5: The Actuator Cartel’s Endgame — implications, challenges, and what comes next

If you found this useful, consider subscribing. I write about the supply chains, the components, and the quiet industrial stories that drive technology forward — the stuff that doesn’t make the front page but determines whether the future actually arrives on time.

Disclosure: This is not investment advice. I’m just someone who finds supply chains weirdly fascinating and thinks the actuator story is one of the more interesting industrial dynamics unfolding right now. Do your own research, talk to people who actually know what they’re doing, and please don’t YOLO your retirement into Japanese precision gearbox stocks because some newsletter writer got excited about robots.