Actuators Part 4: Tesla, Figure, and Unitree’s Supplier Wars

Three companies, three procurement strategies. Whoever controls the actuator supply chain will dictate the winners.

The Actuator Cartel — A 5-Part Series

1. Who Controls the Robot Muscle Supply Chain

2. From Harmonic Drives to Torque Motors

3. The Chinese Are Coming

4. Tesla, Figure, and Unitree’s Supplier Wars

5. The Actuator Cartel’s Endgame

The humanoid robot industry is not fighting over AI models. It’s fighting over supply chains for electric motors the size of a fist. The reality is that whoever controls the actuator supply chain controls the manufacturing cost curve, and whoever controls manufacturing cost controls the TAM. The market is mispricing who wins this fight.

In October 2025, Tesla reportedly dropped a $685 million order on Hangzhou-based Sanhua Intelligent Controls for linear actuators. At an estimated $950–$1,200 per actuator, that covers roughly 600,000–720,000 individual units, enough for approximately 43,000–51,000 Optimus robots at 14 linear actuators per body. Sanhua denied the specific number, they always do, but the A-share market didn’t care. Sanhua’s stock hit the daily limit. The supply chain had spoken: the actuator arms race has moved from engineering labs to procurement contracts.

A single Optimus Gen 3 uses 14 linear actuators in the body and 25 coreless-motor-driven actuators per hand (50 total). At 43,000–51,000 robots worth of linear actuators in a single procurement batch, the math implies Tesla is tooling for volumes that make the 50,000–100,000 unit 2026 target look conservative.

But the real story isn’t the order size. It’s what the order reveals about procurement philosophy. Three companies. Tesla, Figure, and Unitree, are pursuing three radically different actuator procurement strategies. Each one encodes a bet about where the industry’s cost structure settles. Each one produces different winners in the public markets. And each one has a hidden fragility that the consensus is ignoring.

The Cost Architecture of a Humanoid Joint

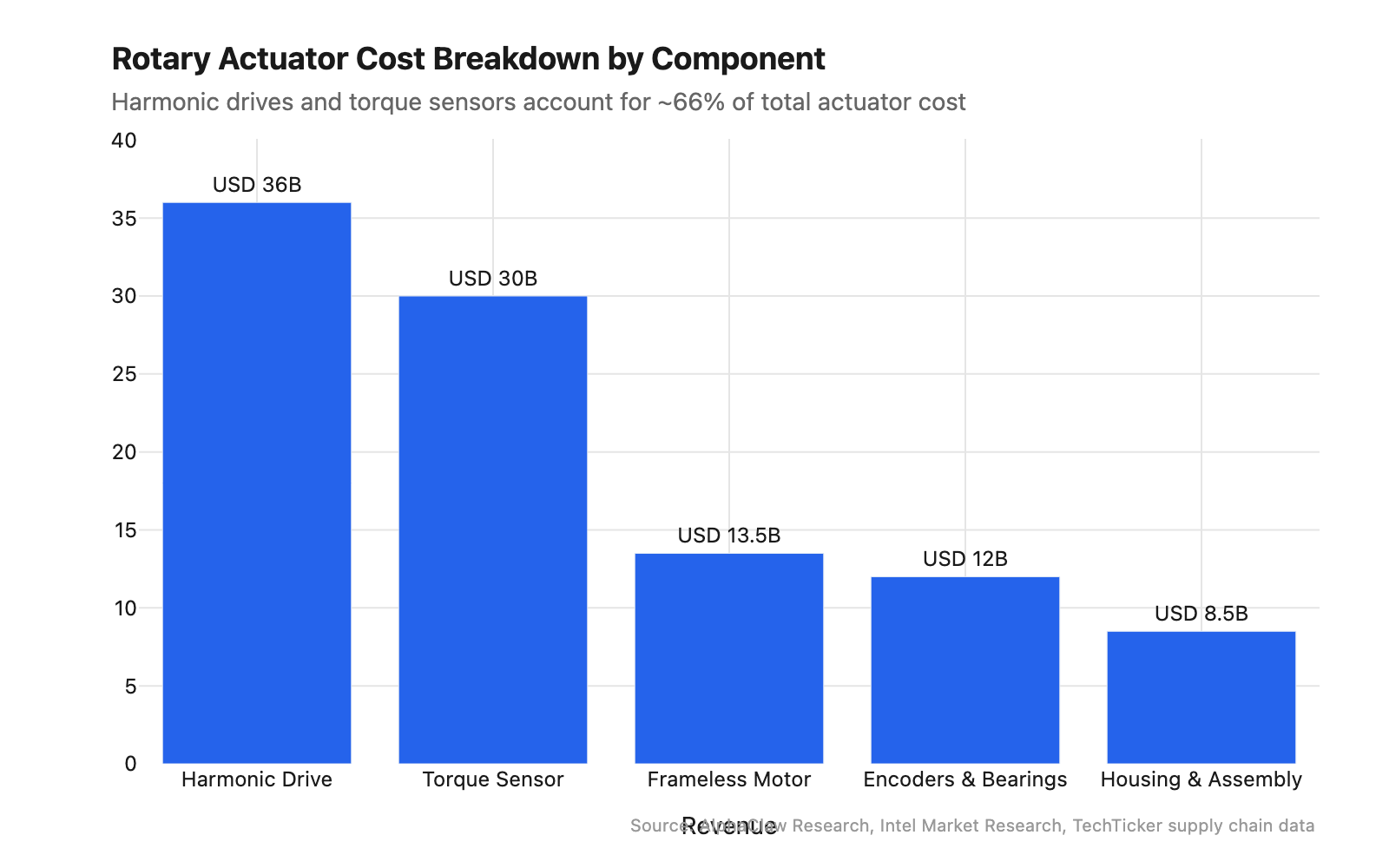

First, let’s talk about what’s actually inside a humanoid actuator. According to Intel Market Research supply chain analysis, the bill of materials for a premium rotary actuator breaks down as follows: harmonic drive reducer (~36% of cost), torque sensor (~30%), frameless torque motor (~13.5%), with encoders, bearings, and housing making up the remainder. Together, these three components account for roughly 80% of the actuator’s total cost. Premium rotary actuators for humanoid robots currently cost between $500 and $5,000 per unit depending on torque density and precision requirements. Linear actuators, which use planetary roller screws instead of harmonic drives, run $400–$1,200 per unit at current volumes.

An Optimus-class humanoid with 28 body actuators and 50 hand actuators (25 per hand) has an actuator BOM in the $28,000–$45,000 range at today’s component pricing. At Tesla’s target of $20,000–$25,000 per complete robot, the actuator cost needs to collapse by roughly 60–70% from current spot prices. That isn’t a design problem. It’s a procurement problem. And it’s why the supplier strategy matters more than the motor topology.

Precision gearing and sensing account for two-thirds of actuator cost, that's where the margin lives.

Behind the paywall: Here are the numbers. At 50,000 units per year, the actuator BOM for a single Optimus-class humanoid runs $28,000–$45,000 at current component pricing. Three Chinese suppliers control over 60% of that bill of materials. And one procurement decision, vertical integration versus supply chain arbitrage, will determine who captures the margin. Below, we break down exactly how Tesla, Figure, and Unitree are placing their bets, which strategy produces structural cost advantage at scale, and which three public-market component suppliers stand to benefit regardless of who builds the most robots.

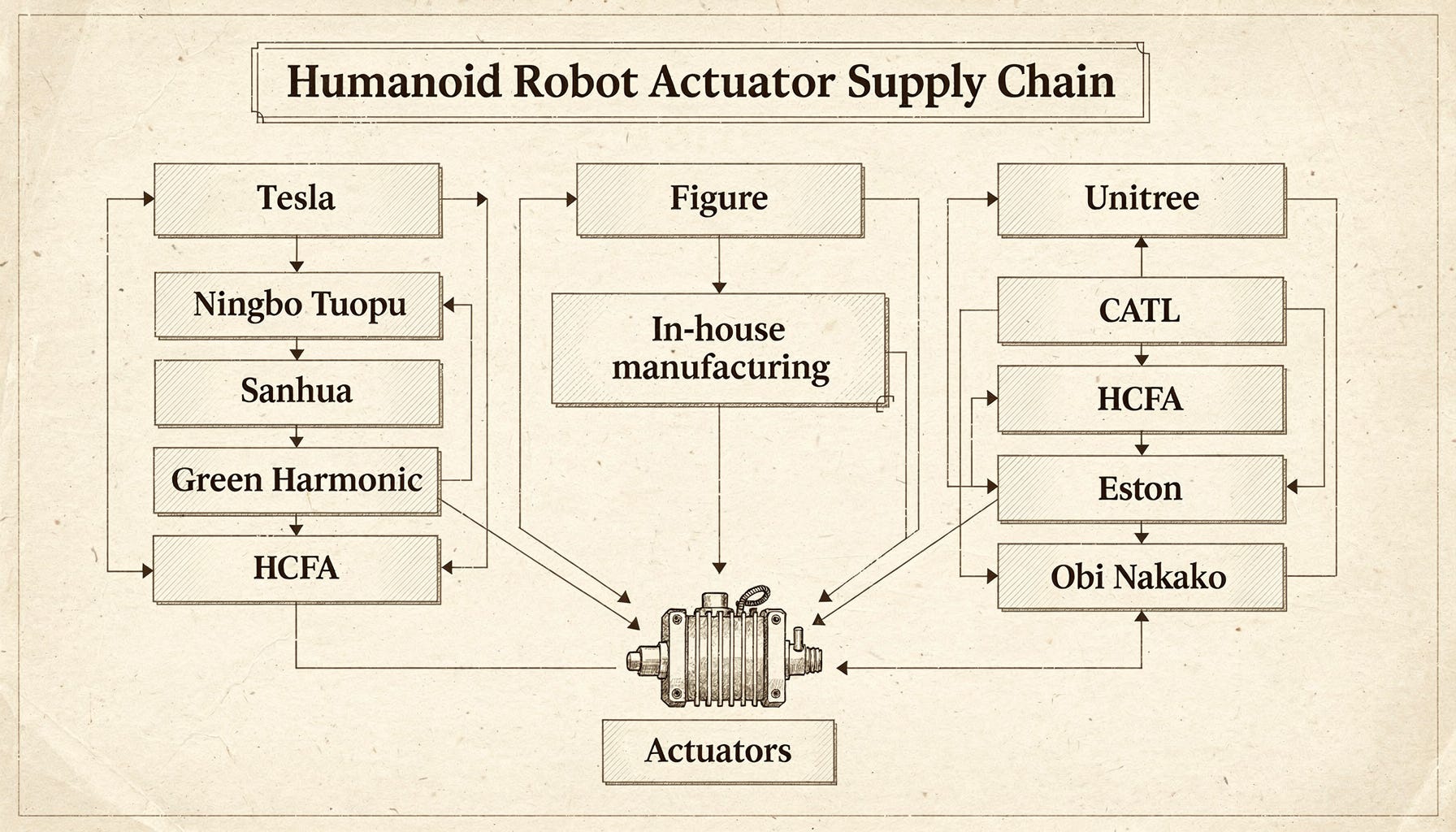

Tesla: The Hybrid Empire

Tesla’s approach is best described as a hybrid: design in-house, manufacture through captive Chinese suppliers, assemble in Austin. It is neither pure vertical integration nor pure outsourcing. It’s the automotive supply chain playbook applied to robotics, and it’s working.

The key partnerships tell the story. Ningbo Tuopu Group (601689) is the exclusive supplier of rotary actuators to Tesla Optimus. Tuopu wasn’t a robotics company, it was an automotive chassis and suspension supplier that had been in Tesla’s EV supply chain since 2016. When Tesla needed someone who could design frameless torque motors and integrate harmonic reducers at automotive scale and automotive cost, Tuopu was the obvious candidate. Mass production of Tuopu’s rotary actuators began in 2024, with a single-vehicle value exceeding ¥10,000 (~$1,400).

Sanhua Intelligent Control (002050) got the linear actuator side. Sanhua controls the #1 global market share in electronic expansion valves and over 35% of the broader thermal management components market, a completely different product category, but its precision manufacturing of small electromechanical assemblies transferred directly to planetary roller screw integration. The $685 million order in October 2025 wasn’t a gamble on an unproven supplier. It was capacity reservation on a partner that had already proven it could hit automotive quality at automotive cycle times.

Behind both of these sits Green Harmonic (688017), the domestic Chinese harmonic reducer manufacturer that has broken the monopoly of Japan’s Harmonic Drive Systems. Green Harmonic now controls over 60% of China’s harmonic reducer market and is the primary harmonic reducer supplier for Tesla Optimus. Supply chain analysis shows Tesla is Green Harmonic’s largest customer by volume, though exact revenue percentages are not publicly disclosed. As we detailed in our actuator cartel supply chain mapping, when we talk about supply chain concentration risk in humanoid robotics, we’re really talking about one factory in Suzhou.

Actuators account for approximately 56% of the total value of major components in Tesla Optimus, per supply chain analysis from Yicai Global and Futu Securities.

HCFA Technology (688320) supplies frameless torque motors to both the Tesla chain and the Huawei chain, as one of the leading domestic frameless torque motor manufacturers with significant market share. Keli Sensing (603662), the only Chinese manufacturer of six-dimensional torque sensors, benchmarked against ATI in the United States, has been sampled to Huawei and is seeking Tesla qualification. The pattern is clear: Tesla is building a China-dependent actuator supply chain that looks increasingly like its China-dependent battery supply chain circa 2019.

The fragility here is geographic concentration. China controls roughly 90% of global NdFeB rare earth magnet supply, and export licenses have been required since April 2025. Each Optimus requires approximately 3.5 kg of NdFeB magnets. At 100,000 units, that’s 350 metric tons, a rounding error in the global rare earth market. At 10 million units, it’s a strategic vulnerability. The same supply chain that gives Tesla cost advantage today is the one that creates single-point-of-failure risk at scale. Our supply chain model shows that a rare earth export disruption would hit Tesla’s actuator cost curve harder than any competitor’s.

Three procurement strategies, three supply chain architectures, and no consensus on which approach produces structural cost advantage at scale.

Figure: The Full Stack Gambit

Figure AI is doing something fundamentally different, and more expensive in the near term. The company designs everything in-house: motors, actuators, sensors, battery systems, embedded software, firmware, controls. Brett Adcock has been explicit: “Figure is vertically integrated and designs everything in house.” This is not a procurement strategy. It’s a declaration of war on the supplier concept itself.