Materials Part 4: Who Profits When Robots Need Magnets

The supply gap is the trade. Demand hits before Western capacity comes online.

The Materials Stack — A 4-Part Series

1. The Magnet Nobody Talks About

2. The Engineering Case for NdFeB

3. The China Chokepoint

4. Who Profits When Robots Need Magnets

In September 2010, a Chinese fishing trawler collided with Japanese coast guard vessels near the Senkaku Islands. China restricted rare earth exports to Japan. Neodymium oxide went from under $10/kg to nearly $239/kg. Molycorp went public at $14, hit $70 by early 2011. Lynas saw similar euphoria.

Then it collapsed. China backed off. The WTO ruled against Beijing in 2014. Prices cratered. Molycorp filed for bankruptcy in 2015. The entire rare earth thesis of the early 2010s turned out to be a geopolitical trade masquerading as a structural one.

The question before we talk about NdFeB magnet stocks today: is this time different?

I think it is. But the bear case deserves steelmanning first.

If this analysis is useful, subscribe for free to follow the full NdFeB series.

The 2010 Trade Failed. This One Might Not.

The 2010 analogy has a flaw most analysts miss: they think the lesson is “China weaponized rare earths and the world built alternatives.” The real lesson is that the world started to build alternatives, the crisis passed, and everyone lost interest. Lynas got its mine running. Molycorp got Mountain Pass back online. Neither became competitive with Chinese producers on cost. When prices collapsed, the economics evaporated.

The structural dependency never resolved. It stopped being urgent. Sixteen years later, China’s share of rare earth processing is higher than in 2010.

In April 2025, China imposed export controls on finished NdFeB magnets, not just raw ores. Automakers shut down production lines. The 2010 crisis was about export quotas on raw materials, resolved by alternative supply coming online and WTO pressure. This time, China restricts finished magnets, and the WTO can’t do much about controls framed as national security measures. The legal resolution from 2010 doesn’t apply.

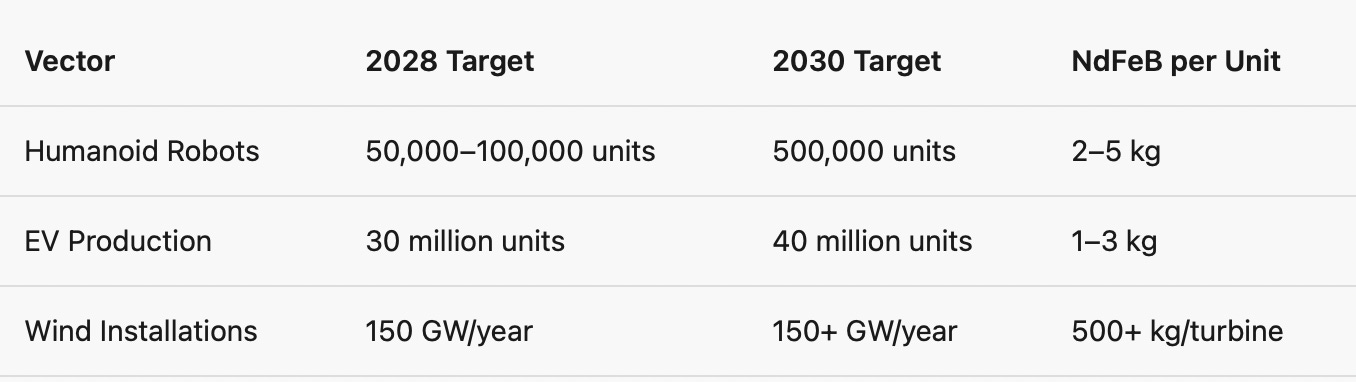

The demand profile is also different. In 2010, the rare earth trade was a bet on a policy dispute. Today it’s a bet on physics. You cannot substitute away from NdFeB in humanoid robots. Ferrite magnets are 11.5 times weaker. Iron nitride magnets are at TRL 2 or 3, a decade from commercialization. Each humanoid robot needs 28 to 76 motors, each requiring NdFeB magnets, totaling 1 to 5 kilograms per unit.

The Demand Curve Is Real

The numbers stack fast across three vectors.

The EV transition alone would strain non-China supply. Adding robotics creates a demand profile the Western supply chain cannot serve.

The Timing Mismatch Is the Trade

Non-China NdFeB capacity today is roughly 12,000 to 18,000 tonnes per year. By 2028, it might reach 25,000 to 35,000. By 2030, optimistically 35,000 to 50,000.

Humanoid robot demand is small in absolute terms: 100 to 500 tonnes by 2028, maybe 1,000 to 2,500 by 2030. The squeeze isn’t about volume. It’s about priority.

Defense contractors and major EV OEMs will lock up most non-China capacity through long-term contracts. They’re already doing it. Humanoid robot companies are late to the procurement queue, startups competing with established industrial giants for every kilogram.

Chinese humanoid OEMs like Unitree, UBTECH, and Tesla’s Shanghai operations have direct access to Chinese magnet supply. American and European humanoid companies don’t. The supply gap isn’t just an investment opportunity; it’s a competitive moat for Chinese robotics.

The supply gap is real. The timing mismatch is real. The demand curve is locked in by physics, not policy. The question is not whether this trade works — it’s who captures the value when it does.

Below, I break down the only mine-to-magnet bet in the Western world, the boring alternative that might be smarter, why Japan’s position is weaker than it looks, the bear cases I find most convincing, and the specific trade setup I’d consider if I were allocating capital to this thesis today. Three companies. One clear winner. Two that might surprise you.