Actuators Part 5: The Oligopoly's Endgame

When Tesla builds its own motors, China prices them at cost, and the old guard has nowhere left to hide.

The Actuator Cartel — A 5-Part Series

1. Who Controls the Robot Muscle Supply Chain

2. From Harmonic Drives to Torque Motors

3. The Chinese Are Coming

4. Tesla, Figure, and Unitree’s Supplier Wars

5. The Actuator Cartel’s Endgame

In 1999, two Japanese companies. Harmonic Drive Systems and Nabtesco, made a quiet agreement. Harmonic Drive would focus on smaller, high-precision harmonic reducers for the wrist joints and elbows of industrial robots. Nabtesco would focus on larger, high-torque RV reducers for the shoulders and hips. Together, they divided the global precision reducer market between them, a gentleman’s arrangement that held for nearly two decades. If you wanted to build a robot that moved precisely, you bought from one of these two companies. End of story.

That agreement was dissolved in 2022. Nabtesco sold its approximately 19% stake in Harmonic Drive Systems by early 2025, netting roughly $357 million in the process. The two companies, which had been cross-shareholders and strategic partners since 2005, are now independent competitors in a market that’s about to get dramatically bigger, and dramatically more competitive. that timing tells you everything you need to know about where this industry is heading.

the endgame. Over the past week, we’ve traced the actuator supply chain from its origins in a 1955 patent by C. Walton Musser, through forty years of Japanese manufacturing dominance, to the Chinese disruption that’s now remaking the competitive landscape. Amanda J mapped the bottleneck in Part 1. I traced the technology arc from harmonic drives to torque motors in Part 2. Phil D showed us the Chinese market share surge in Part 3 and the procurement wars between Tesla, Figure, and Unitree in Part 4. Now I want to synthesize all of that into a single question: who wins, who loses, and what do you do about it?

the answer has three parts. But before I get to the investment thesis, let’s be precise about what we’re actually looking at, because the numbers matter, and in my experience, most of the market commentary on the actuator supply chain is about five years behind the data.

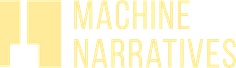

This matters because the precision reducer oligopoly isn’t one company controlling 85% of the market, as some earlier analyses suggested. It’s more nuanced, and in some ways, more interesting. What we actually have is a market dominated by roughly five players, with the top two (HDSI and Nabtesco) holding a combined ~60% share of the high-end precision reducer market for robotics applications, and a third Japanese player (Nidec-Shimpo) adding another ~12%. The Chinese challengers. Green Harmonic, Leaderdrive, Laifual, and a dozen smaller players, have collectively grown from under 10% in 2020 to somewhere around 30% today.

Figure 1: Estimated precision reducer market share in robotics applications, early 2026. Japanese incumbents still hold roughly 70% combined, but the direction of travel is clear. Source: Machine Narrative Research estimates.

HDSI is the clear leader in harmonic drives specifically, the smaller, higher-precision reducers used in robot wrists, elbows, and increasingly, humanoid hand joints. I'd estimate their share of the high-end harmonic drive market at roughly 60%, though exact numbers are hard to come by since the market isn't tracked by any single authoritative source. Nabtesco dominates RV reducers, the larger, higher-torque gearboxes for shoulder and hip joints. The distinction matters because the humanoid robot buildout is likely to require both types: harmonic drives for the dozens of small joints in the hands and wrists, RV reducers for the larger load-bearing joints in the arms and legs.

The Rare Earth Trap

Let me pause here and talk about something that I think gets lost in most supply chain analyses, because it sits one layer deeper than the gearboxes and the torque motors. Every precision actuator, whether it uses a harmonic drive, a planetary gear, or a direct-drive torque motor, depends on permanent magnets. Specifically, neodymium-iron-boron (NdFeB) magnets, the most powerful commercially available permanent magnets in the world. And China controls roughly 90% of the global supply chain for NdFeB magnet manufacturing.

This is not a mining story. The rare earth elements themselves, neodymium, praseodymium, dysprosium, are mined in multiple countries, including the United States (Mountain Pass in California), Australia (Lynas’s Mount Weld), and Myanmar. The bottleneck is in the midstream processing: separating the oxides, producing the alloys, and sintering the finished magnets. That processing infrastructure took China roughly fifteen years to build, and it cannot be replicated quickly. The US, Australia, and Canada are all investing in domestic processing capacity, but even under the most optimistic timelines, meaningful non-Chinese NdFeB magnet production is five to seven years away.

In April 2025, China imposed new export controls on selected rare earth magnets and separation technologies, citing national security concerns. The rules require export licenses for a range of rare earth products, including NdFeB magnet materials. Starting December 1, 2025, the controls were extended extraterritorially, meaning overseas entities using Chinese rare earth processing technologies also need licenses. This is not a hypothetical risk. It’s an active policy framework that can be tightened at any time.

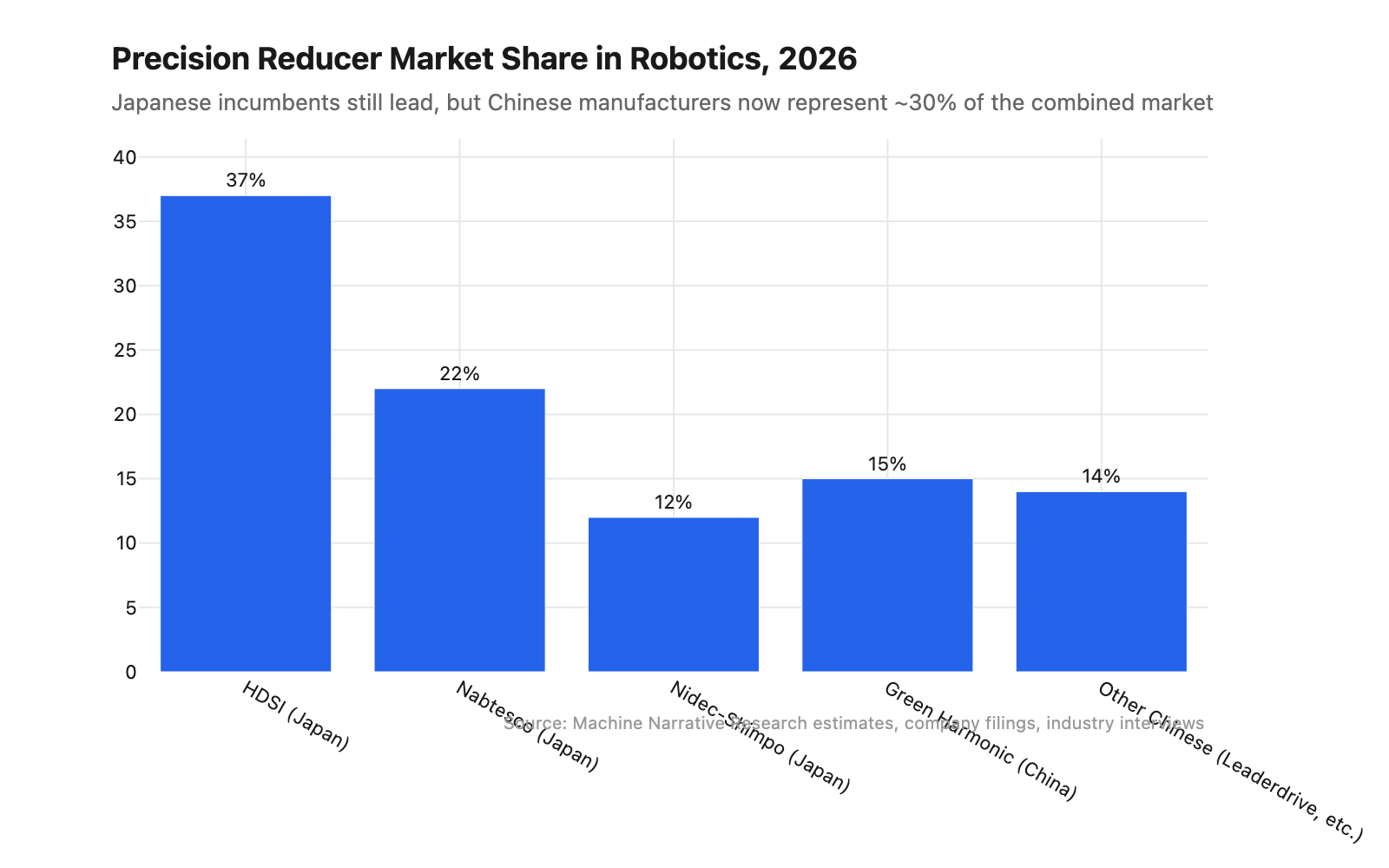

Figure 2: Humanoid robot NdFeB magnet demand as a percentage of global production, 2025–2030F. Today it’s a rounding error (0.03%). By 2030, at 1.2 million robots, it becomes a meaningful demand driver. Source: Adamas Intelligence, Tianfeng Securities, Machine Narrative Research estimates.

Each humanoid robot requires approximately 3.5 kilograms of NdFeB magnets across its actuators. At 50,000 robots, roughly the midpoint of consensus 2026 estimates, that’s about 175 metric tons, or less than 0.1% of global NdFeB production. Nobody in the rare earth industry loses sleep over 175 tons. But the math changes quickly. At one million robots, you need 3,500 metric tons. At ten million. Musk’s stated ambition for Optimus, you’d need 35,000 metric tons, which would represent roughly 14% of current global production. That’s not a rounding error anymore. That’s a market-moving quantity of a material where one country controls the processing infrastructure.

this is the underappreciated risk in the actuator supply chain thesis. Everyone focuses on the gearboxes, who makes the best harmonic drive, who’s got the Tesla contract, whether torque motors will displace gears entirely. But all of those debates assume the raw materials are available. The rare earth trap means that even if you solve the gearbox problem, even if you build the factory and qualify the supplier and lock in the price, you’re still dependent on a single country for the magnets that make every actuator work. That dependency is not diversifiable in under five years. It might not be diversifiable in under ten.

The Chinese Disruption, In Context

Phil D laid out the numbers in Part 3 with admirable precision. Chinese harmonic drive manufacturers have grown from under 10% market share to roughly 30% in five years, with Green Harmonic leading the charge at 12–18% and growing. I want to add some context to those numbers, because I think the pattern matters as much as the level.

Green Harmonic (688017.SH) was founded in 2011 by a pair of brothers in Suzhou. Their first products were, by most accounts, not competitive with Japanese harmonic drives in terms of precision or durability. But they were 40–60% cheaper, and for a Chinese industrial robot manufacturer trying to build a cost-competitive product, that price difference was the difference between viable and non-viable. Over the next decade, Green Harmonic improved its quality steadily, not through any single breakthrough, but through the same grinding, iterative refinement that Japanese manufacturers had used in the 1980s and 1990s. By 2023, their products were good enough for Tesla to qualify them as the primary harmonic reducer supplier for Optimus.

The economics are instructive, and they invert the conventional narrative. HDSI’s gross margins have compressed to approximately 27% as of FY2024. Green Harmonic’s gross margins are approximately 37.5%, a full ten percentage points higher. The Chinese challenger has better margins than the Japanese market leader, and it’s selling at a 40–60% discount. That is not a healthy competitive dynamic for the incumbent. A company with 37.5% gross margins and a large discount to the market leader has room to keep cutting prices. A company with 27% margins and declining revenue does not.

“The challenger has better margins than the market leader and charges 40–60% less. That’s not a competitive dynamic. That’s a countdown.”

The other Chinese players. Leaderdrive, Laifual, and a growing number of smaller manufacturers, are collectively growing faster than any Japanese incumbent. Their products are still primarily sold into the Chinese domestic market, where industrial policy actively favors local suppliers. But the moment a Western humanoid OEM qualifies a second-source Chinese harmonic reducer supplier, the pricing umbrella that supports Japanese margins collapses entirely. that moment is coming within 2–3 years, not 5–10.

I should be fair here. The Japanese incumbents are not passive. HDSI has launched integrated motor-gearbox modules, essentially a harmonic drive with a built-in torque motor, that they’re marketing as a drop-in solution for humanoid robot joints. Nabtesco is expanding RV reducer capacity with humanoid-specific product lines. Nidec-Shimpo is leveraging Nidec’s broader motor expertise to offer bundled actuator packages. These are smart moves, and they reflect the kind of thoughtful, long-term strategic thinking that Japanese industrial companies are famous for. But I think the historical parallel is instructive here, and it’s not a comforting one for the incumbents.

The Solar Panel Parallel

In 2005, Japanese and German manufacturers. Sharp, Kyocera, Q-Cells, dominated the global solar panel market with a combined share of roughly 70%. Their products were premium. Their manufacturing was world-class. Their institutional knowledge was measured in decades. Over the next ten years, Chinese manufacturers. Longi, Trina, Jinko, entered with 30–40% lower prices, government-backed capacity expansion, and an aggressive scaling strategy that prioritized market share over near-term margins.

The incumbents didn’t stand still. They improved their technology continuously. Their products remained, by many objective measures, superior. But by 2015, Chinese companies held over 60% of global solar panel production. Japanese share collapsed from roughly 50% to under 10%. The premium product didn’t lose on quality, it lost on cost, in a market where “good enough” was, in fact, good enough.

The harmonic drive market is smaller, roughly $5–7 billion globally compared to solar’s $200+ billion, but the structural dynamics are identical. A premium incumbent with high margins. A challenger entering at 40–60% lower prices with state-supported capacity expansion. An end-customer base under constant pressure to reduce bill-of-materials costs. And a “good enough” quality threshold that, for the fastest-growing applications, is lower than the incumbents would like it to be.

Not to be alarmist, but I think the precision reducer market is about five years into a ten-year disruption that ends the same way the solar disruption ended: with Chinese manufacturers controlling the majority of global production, Japanese incumbents retreating to the highest-precision, highest-certification niches, and a fundamentally restructured competitive landscape that nobody in Nagano Prefecture wanted but that the economics made inevitable.