The Agility IPO: $2.5 Billion for 100 Robots

The first humanoid to go public. Three squeezes say the price doesn’t work.

Agility Robotics has shipped roughly 100 robots in its entire history. The SPAC, announced June 24, 2026, values the company at $2.5 billion. That’s $25 million per robot shipped. Something has to give.

So today I want to talk about whether the first humanoid robot IPO makes any sense. Not the hype. Not the TAM projections Goldman is putting out. The actual arithmetic of building a walking robot at scale, and what it means for a company trying to go from artisanal assembly to mass production in a handful of years.

What Agility Is Selling

Digit is a bipedal warehouse robot designed to move totes in distribution centers. Five feet tall, roughly 100 pounds, 35 pounds of cargo capacity. Agility doesn’t sell Digit outright. The go-to-market is RaaS, robotics as a service, at $8,000 to $10,000 per month. That’s $96,000 to $120,000 a year in operating expense for the customer, no upfront capital outlay.

The RaaS model is clever. It lowers the adoption barrier for mid-size warehouse operators who can’t write a $250,000 check for an unproven robot but can absorb $8,000 a month in opex during peak season. Digit has moved over 100,000 totes in live commercial deployment with GXO Logistics and Amazon, which is a meaningful proof point for operational maturity.

But 100 robots in nine years is not a production ramp. It’s a pilot program. The market is pricing this company as if 100 will become 50,000. Time to check the arithmetic.

The Three Things You Have to Believe

To justify $2.5 billion, you need to believe three things: Agility can produce 50,000 cumulative units by 2030, sell them at roughly $120,000 per unit in annual RaaS revenue, and do it at a BOM cost of $25,000 to $35,000 per robot.

Those are the three inputs. Quantity, price, cost. Everything else is derived.

Let me steelman each one before we stress-test them.

Quantity: 50,000 cumulative units by 2030. Not 50,000 in a single year. That’s 50,000 total, running at maximum factory output for four to five consecutive years. RoboFab, Agility’s purpose-built facility in Salem, Oregon, is designed to scale to 10,000 units per year. There are no public announcements of additional manufacturing sites or contract manufacturing partnerships. RoboFab is it.

Price: $120,000 per unit per year in RaaS revenue. That’s the midpoint of the $96,000 to $120,000 annual range at the $8,000 to $10,000 monthly rate. This assumes customers pay consistently and the robots stay operational enough to justify the fee. At scale, list prices for the hardware itself would need to hold above $100,000 to $150,000 if Agility ever shifts to direct sales.

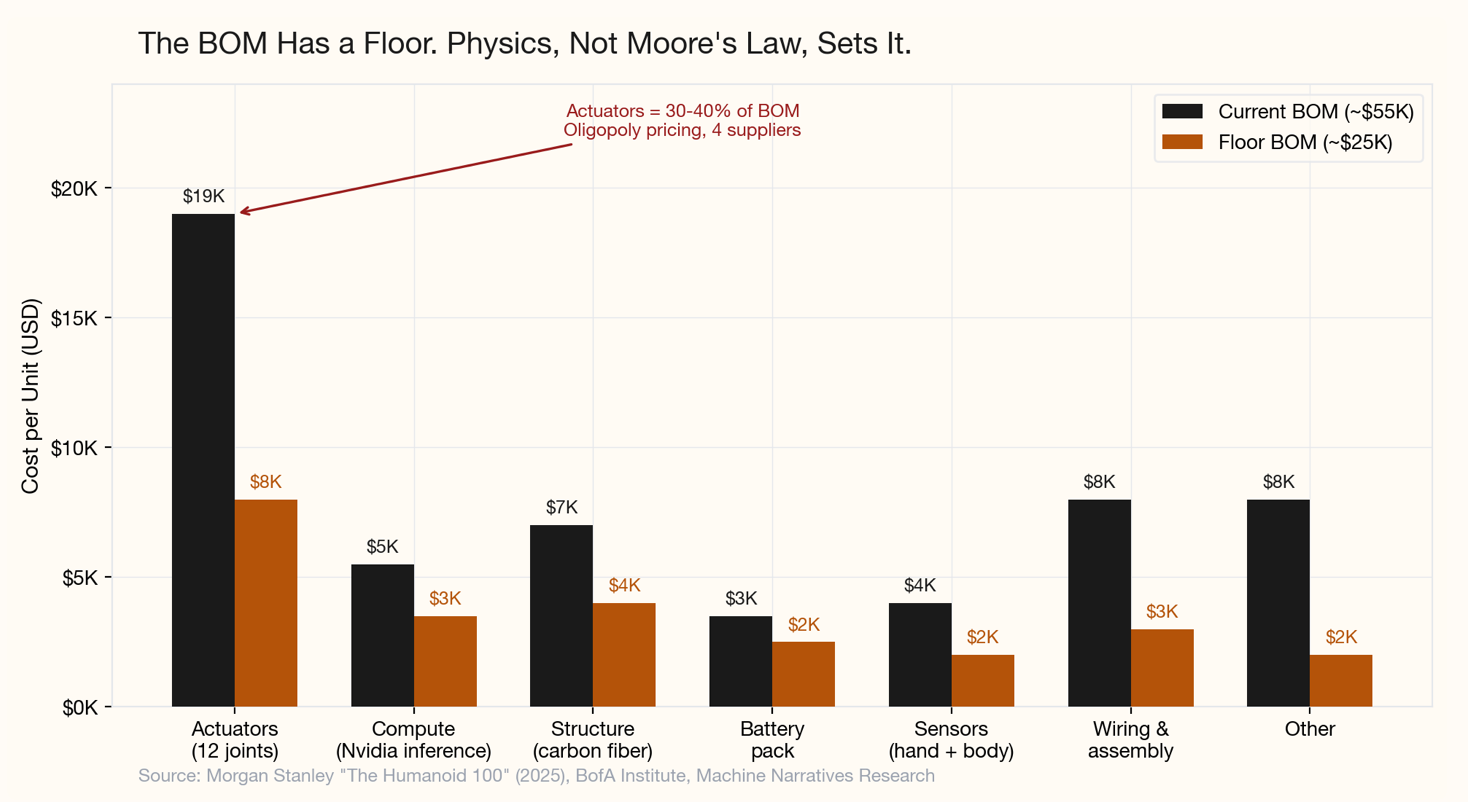

BOM cost: $25,000 to $35,000 per unit at scale. Morgan Stanley pegs the current BOM at $50,000 to $60,000. Getting to $25,000 to $35,000 requires a 40 to 50 percent decline through volume manufacturing, actuator standardization, and supply chain optimization. Bank of America projected BOM could drop to $17,000 by 2030, but I think that’s optimistic. The realistic floor is $25,000 to $35,000.

Stack those three inputs and you get a picture of a company that needs to quintuple its production rate from a single factory, while simultaneously cutting the cost of building each robot in half. That’s the bet.

Now the question becomes whether each input survives contact with reality.

Squeeze 1: The Factory

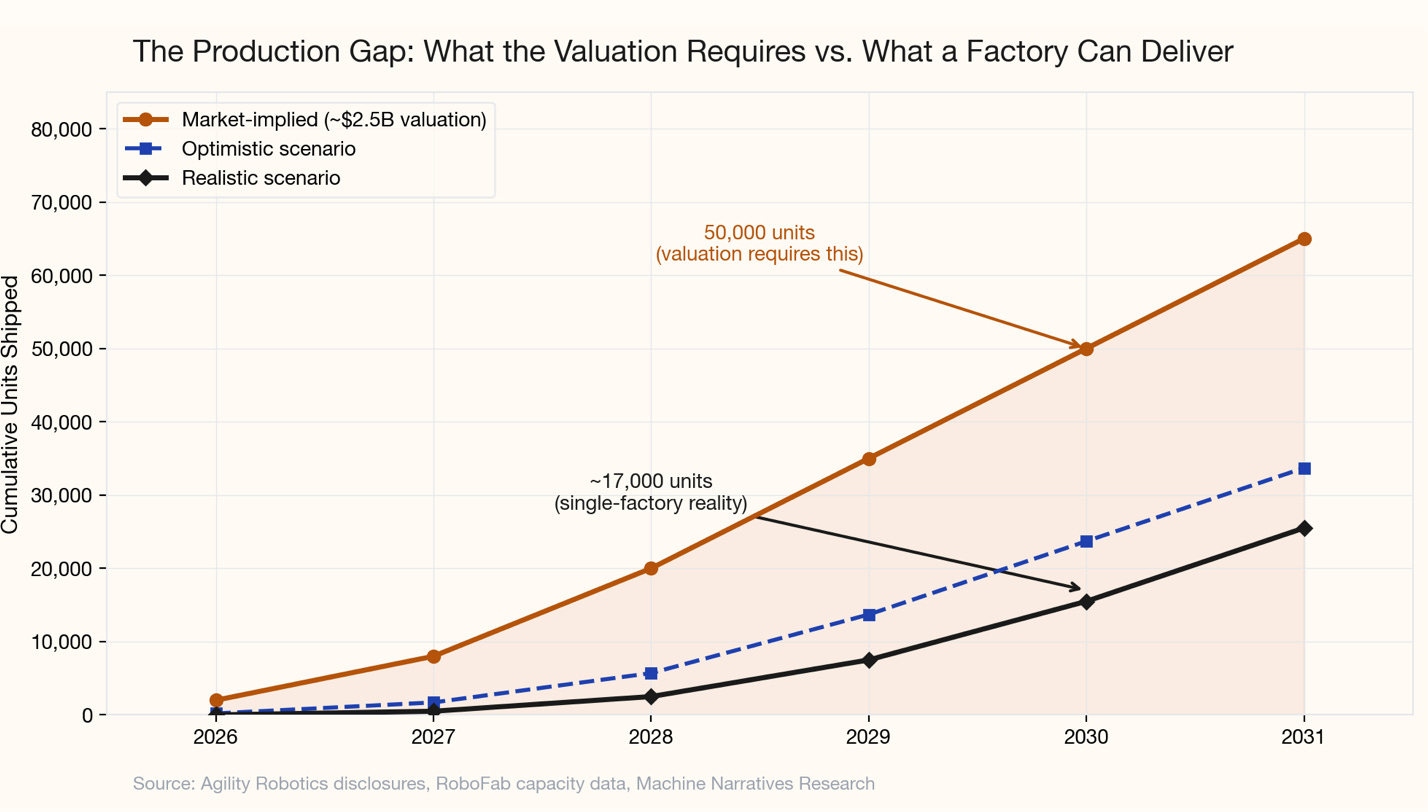

RoboFab is designed to scale to a maximum of 10,000 units per year. At maximum capacity, reaching 50,000 cumulative units requires five consecutive years of flat-out production starting from essentially zero today. The facility is still being built out. Even the most optimistic internal projections don’t claim 10,000 units per year before 2029.

I’d argue the closest historical parallel is Tesla’s Model S ramp, and it was brutal. In 2012, Tesla delivered 2,650 Model S sedans. By 2015, they were over 50,000 annually. That’s roughly a 19x increase in three years. It nearly bankrupted the company. Elon Musk has said publicly that Tesla was within weeks of running out of cash during the 2013 ramp. They needed multiple emergency funding rounds.

Tesla had something Agility doesn’t: the NUMMI factory in Fremont, a facility designed for mass automotive production since 1984. It had paint shops, stamping presses, welding robots, and assembly lines that could be retooled. Tesla bought it for $42 million in 2010. RoboFab is being purpose-built for humanoid robot production, which means Agility is simultaneously designing the product, the manufacturing process, and the factory itself. Three hard problems instead of one.

Here’s the timeline arithmetic. If RoboFab starts producing in 2027, which is optimistic, and ramps to 2,000 units in year one, 5,000 in year two, and 10,000 by year three, you’re looking at roughly 17,000 cumulative units by 2030. That’s a third of the 50,000 target the valuation requires. To hit 50,000 by 2030, Agility would need to start producing in 2026, hit 10,000 annually by 2028, and maintain that rate for three straight years. The ramp would need to be faster than Tesla’s, and Tesla had a factory designed for mass production.

The arithmetic is stark. You’re betting that a company that has shipped 100 robots can go from artisanal assembly to maximum factory output in a handful of years. Tesla did something similar. Tesla also almost died doing it, and they had infrastructure Agility can only dream of.

Squeeze 2: The BOM Floor

The BOM trajectory is the most important number in this entire thesis, and the part that gets the least attention.

At the $25,000 to $35,000 BOM range I laid out in the valuation section, the unit economics work. At $120,000 in annual RaaS revenue per robot, you’re generating enough gross profit to cover deployment, maintenance, and overhead while still contributing to growth. But that’s at scale. At the current $50,000 to $60,000 BOM, the math is much tighter.

The reason BOM has a floor comes down to physics and geopolitics, not engineering cleverness. I want to spend some time here because this is where most bull cases fall apart. People wave their hands about learning curves and scale economies without looking at what’s actually inside the robot.

Actuators alone represent 30 to 40 percent of the bill of materials. Each robot needs 12 joints, each with a harmonic reducer and servo motor, running $6,000 to $12,000 at current volumes. Four companies control the critical actuator components. That oligopoly doesn’t dissolve because you order more units. Volume manufacturing helps, but the supply chain concentration means pricing power stays with the suppliers, not the robot maker.

Structural materials, carbon fiber composites accounting for 10 to 20 percent of BOM, have their own concentrated supply chains. The compute stack, Nvidia inference hardware because there’s no alternative at this performance tier, adds another layer of cost that Nvidia has no incentive to compress. Every motor needs neodymium magnets from a supply chain where China controls 94 percent of NdFeB production.

None of this follows Moore’s Law. None of it compresses 10x every decade. The components inside a humanoid robot are governed by the same physics as the components inside a car, and car BOMs haven’t dropped 50 percent in five years either.

The hand alone is a microcosm of the problem. Forty-plus force and tactile sensors at $800 to $2,000 per robot, with no volume manufacturing path for most of them. The sensors are custom. The suppliers are small. The demand signal from 100 robots doesn’t move the needle on their production economics.

There’s another dimension that rarely gets discussed: the Chinese vs. non-Chinese BOM differential. Chinese competitors like Unitree are building humanoid robots at BOM costs of roughly $46,000. Agility’s estimated BOM sits at $50,000 to $60,000. That differential isn’t dramatic at first glance, but it compounds at scale. Agility’s 80 percent US-sourced supply chain reduces geopolitical risk but locks in a higher cost floor than Chinese competitors face.

As volume manufacturing kicks in and actuator designs standardize, those costs should decline meaningfully, maybe 30 to 40 percent from current levels. But that still leaves you with $4,000 to $8,000 per robot just in actuators. Add $3,000 to $5,000 for compute, $3,000 to $6,000 for structure, $1,500 to $4,000 for the battery, and you’re at $17,000 to $25,000 before you’ve wired a single connector.

The BOM has a floor. That floor sits somewhere between $25,000 and $35,000. Below that floor, you can’t build the robot. Above it, the unit economics start to work at the $120,000 per unit per year RaaS rate. But the floor exists, and it’s dictated by physics and geopolitics, not by software-style scaling laws.

To be clear: Bank of America projects $17,000 by 2030. I think that’s a fantasy. It assumes actuator costs compress by 60 percent, compute costs follow a Moore’s Law curve that Nvidia has no incentive to enable, and structural materials somehow get cheaper despite concentrated supply chains. The realistic range is $25,000 to $35,000, and even getting to $25,000 requires everything to go right.

Squeeze 3: The Competition

The bear case here isn’t about demand. It’s about whether Agility can win the race it’s in.

Let’s look at who else is building.

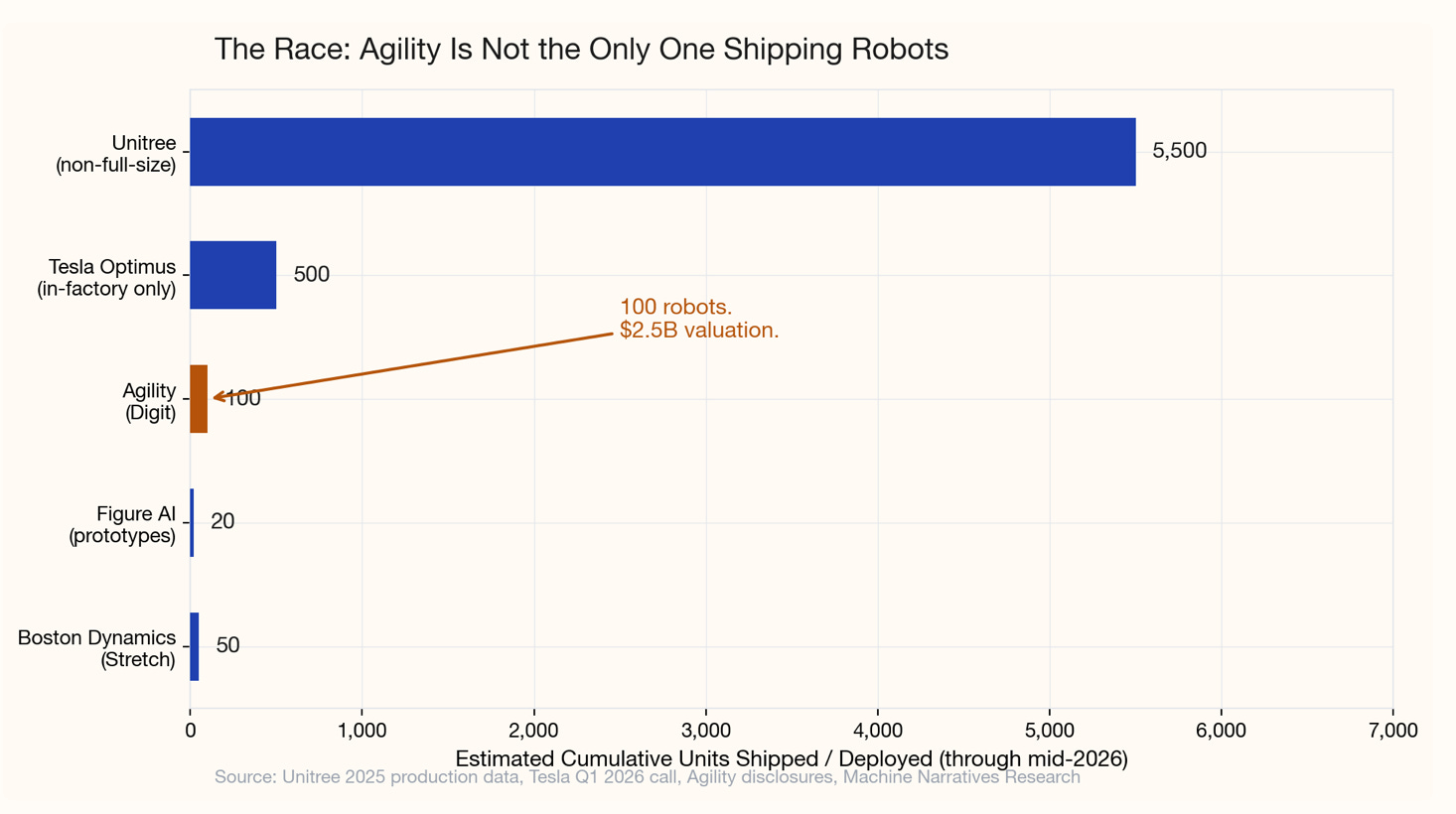

Tesla has announced ambitious Optimus production targets, 5,000 units in 2025, scaling to 50,000 to 100,000 in 2026, but has consistently missed them by enormous margins. As of mid-2026, Tesla has deployed only 300 to 500 Optimus units, almost entirely within its own factories. Musk declined to reaffirm the 2026 target on Tesla’s Q1 2026 earnings call. They’re still leveraging their existing automotive supply chain, established manufacturing infrastructure, and over $25 billion in cumulative AI and robotics investment. Tesla doesn’t need to build a factory from scratch. They have factories. But having factories and actually producing robots at scale are very different things, as the gap between target and reality demonstrates.

Figure AI has raised $745 million with backing from Microsoft, OpenAI, and NVIDIA. They haven’t shipped production units yet, but the capital stack and strategic partnerships give them a runway that most startups can’t match. Boston Dynamics has its electric Atlas program and a 1,000-unit agreement with DHL for its Stretch warehouse robot. Stretch isn’t a humanoid, but it’s competing for the same warehouse budget dollars. And then there’s Unitree, which shipped over 5,500 non-full-size humanoid units in 2025 (mostly to research institutions, with roughly 70 percent exported) and is targeting 20,000 units in 2026.

The competitive dynamics matter because they affect all three inputs in the valuation model. More competitors mean more pressure on the $120,000 per unit per year RaaS rate. More production volume across the industry means actuator suppliers have less incentive to cut prices for any single customer. And more capital flowing into the space means Agility’s first-mover advantage erodes faster.

At the $25,000 to $35,000 BOM floor I described earlier, the unit economics work at $120,000 per year in RaaS revenue. But Unitree is building at $46,000 BOM today, and they’re not standing still. If Chinese competitors get to $30,000 BOM while Agility is at $35,000, the pricing pressure on Agility’s RaaS rate becomes intense. You can’t charge $10,000 a month for a robot that costs the same to build as a competitor’s $6,000-a-month unit.

Agility’s advantages are real but narrow. They have first-mover experience in purpose-built humanoid manufacturing. They have operational deployment data that no one else has at this scale. And they have Amazon and GXO as validation partners. The question is whether that head start matters when Tesla decides to pour automotive-scale resources into the same market.

The window Agility had as the only serious player is closing fast. Two years ago, the humanoid robot market was essentially Boston Dynamics doing backflips on YouTube and Agility quietly building warehouse bots. Now you have Tesla, Figure AI backed by the biggest names in tech, Unitree shipping thousands of units from China, and a dozen other startups burning through venture capital. Agility’s moat is deployment experience, data on how robots fail in real warehouses, what breaks first, how operators actually use the machines. That data is genuinely valuable. But it’s a moat with a timer on it. Every month that Tesla, Figure, and Unitree deploy their own robots, that experiential advantage erodes.

Here’s the uncomfortable question: what happens to the $120,000 per unit per year RaaS rate when Unitree offers a comparable warehouse robot at $6,000 a month? Or when Tesla bundles Optimus with its existing warehouse automation stack? The pricing power assumption in the valuation model requires Agility to maintain premium pricing in an increasingly commoditized market. That’s possible if Digit is genuinely better than the alternatives. It’s not possible if the alternatives are 80 percent as good at 50 percent of the price.

The SPAC Structure

One more thing about the structure of this deal. The SPAC IPO was announced June 24, 2026, at a $2.5 billion valuation. Agility had previously raised a $400 million Series C in March 2025 at a $2.12 billion valuation, so the SPAC represents a modest markup from the last private round.

SPACs provide public market currency for future acquisitions and talent retention. Stock options in a publicly traded company are more liquid than private equity, which matters when you’re trying to recruit engineers away from Tesla and Google.

But the track record for SPAC’d hardware companies is, to put it politely, mixed. Nikola and Lordstown Motors are the cautionary tales everyone invokes, and for good reason. Both promised revolutionary hardware, both went public via SPAC, and both collapsed when the production reality failed to match the investor presentation. Digit actually exists and works, which is already more than Nikola ever had. But the structure carries baggage that investors should be aware of.

There’s also the timing question. Agility is going public at a moment when humanoid robotics hype is near peak levels. Goldman Sachs 6xing their TAM estimate will do that. The SPAC structure means Agility gets public market currency without the scrutiny of a traditional IPO roadshow. That’s good for Agility. It’s less good for investors who want to stress-test the production assumptions before buying in.

Where I Come Out

The bull case is real. The warehouse labor shortage is genuine. Goldman Sachs revised their humanoid TAM estimate upward by 6x, from $6 billion to $38 billion by 2035, and now projects 1.4 million humanoid robot shipments over that period. Digit works. The 100,000 totes moved in live deployment prove operational maturity. GXO and Amazon are validation partners, not science experiments. RaaS lowers adoption barriers. The demand is there.

But the bear case is arithmetic. Three squeezes, each independently problematic, each compounding the others.

Squeeze 1: Volume. The market prices 50,000 cumulative units by 2030. The single-factory constraint yields roughly 17,000. That’s a third of what the valuation requires.

Squeeze 2: BOM cost. The floor sits at $25,000 to $35,000 per robot. At $50,000 to $60,000 today, you need a 40 to 50 percent decline that physics and supply chain concentration make difficult. The BOM doesn’t compress like software.

Squeeze 3: Pricing power. Tesla has factories and $25 billion in investment. Unitree builds at $46,000 BOM. Figure AI has $745 million and the backing of Microsoft, OpenAI, and NVIDIA. The window is closing.

Stack the three squeezes together: a single factory that can produce a third of the required volume, a BOM floor that sits at $25,000 to $35,000 with no Moore’s Law to compress it, and competitors with deeper pockets and lower costs. The market is pricing Agility at roughly 2 to 3x what the supply chain can deliver in the next three years.

My number: if you give Agility every benefit of the doubt — RoboFab starts producing in 2026, hits maximum output by 2029, BOM drops to $25,000, RaaS rate holds at $10,000 a month, and no competitor undercuts them — you get to maybe $1.5 to $2 billion in enterprise value by 2030. That’s the bull case. And it requires everything to go right.

The more realistic scenario: RoboFab starts in 2027, hits 8,000 units per year by 2030, BOM lands at $30,000 to $35,000, and competition compresses the RaaS rate to $7,000 to $8,000 a month. That’s a $600 million to $1 billion company. Still a real business. Still worth building. Just not worth $2.5 billion today.

I think we’re watching the first chapter of the humanoid robot IPO story. Whether it’s a success story or a cautionary tale depends entirely on what happens in Salem, Oregon over the next 36 months. The demand is there. The technology works. The money is available. The only question is whether Agility can actually build the things. And if they can’t, someone else will. The market opportunity doesn’t disappear just because one company stumbles.

Anyways. The humanoid robot market is real. The supply chain constraints are real. And $2.5 billion is a lot of money for 100 robots. Hope everyone has a great day, and I’ll talk to you soon.

Related Reading from Machine Narratives Research:

The Actuator Cartel: Who Controls the Robot Muscle Supply Chain — The hidden chokepoint behind every humanoid robot

The Magnet Nobody Talks About: Why Humanoid Robots Can’t Scale Without NdFeB — Each robot needs 40 motors. Every motor needs rare earth magnets.

The Leg Battery Problem — Why EV batteries fail inside walking machines

The Compute Tax — Nvidia’s toll booth on the robotics revolution

Tesla, Figure, and Unitree’s Supplier Wars — Three companies, three procurement strategies

The Actuator Oligopoly’s Endgame — When Tesla builds its own motors and China prices at cost